DIC 12 2021 P-B ND SIT ECON y POL Part 1 & P 2

ND denounce-neoliberal debacle y propone State-Social + Capit-compet in Eco

ZERO HEDGE ECONOMICS

Neoliberal globalization is over. Financiers know it, they documented with graphics

Quick News 1

THE COMING INFLATION TSUNAMI AND HOW TO PREPARE

How bad could it get and what you can do to protect your portfolio.

====

Quick News 2

IS THE GOLD PRICE SUPPRESSED ON THE COMEX FUTURES EXCHANGE?

From examining the roll data I have found no evidence of price suppression.

====

Do systematic non-fundamental strategies and fundamental stock pickers both need to re-lever at the same time, at ATH’s? What happens when we finally break above $4700? How high can we go in the next 3 weeks?

This time Tyler Durden copy artic from Goldman huge Corp

It comes with the story: This art is so good that is not for you,

II is for members only. This could mean that:

If you don’t have money to pay subscription, you are out.

Zero hedge is one of the best sources for FREE PRESS. Instead of denying

Good INFO Tyler should abstain of publishing that note above. IF Tyler Durden

needs Money he can request voluntary donations. Many people will do it., me too.

….

….

La mariguana de Perú se vende muy cara cerca a museos y teatros de concierto en Paris

VISUALIZING THE HISTORY OF CANNABIS PROHIBITION IN THE US

In 1619, a law was passed in the colony of Virginia which required every single farm to grow cannabis...

….

La marihuana del US se cultiva en los áticos o en labs y no de cara al sol como en la selva de Perú y Brasil. No adquiera por tanto la flor roja -moño rojo (le llamamos) que permite liberar el polen, y auto-reproducir la planta y darle fuerza a las hojas. Aquí en el US le introducen el veneno llamado ‘pasta básica’ (una agua amarilla con químicos que se tira a la basura cuando se procesa la cocaína) e incluso le adhieren adictivos y otros para crear una inmensa planta a la que llaman marihuana. Eso es veneno, no marihuana. La real marihuana no es adictiva ni golpea cuando la fumas. La marihuana real es bien suave y con dos hojitas en un pitillo (papel de arroz) uno puede relajarse todo el tiempo que demora un concierto de música clásica o tomar aire puro echado en el pasto de un parque. La marihuana solo estimula los sentidos humanos al máximo. No crea adicción ni enfermedad alguna. La fumé 3 o 4 veces a la semana durante los 9 meses que viví en la selva peruana. Allí es gratis, pero estaba prohibido traerla a las ciudades de la costa. Te la quitaban los aduaneros y se quedaban con ella. Las francesas si la llevaron hasta Paris y yo no sé cómo. La venden muy caro allí.

====

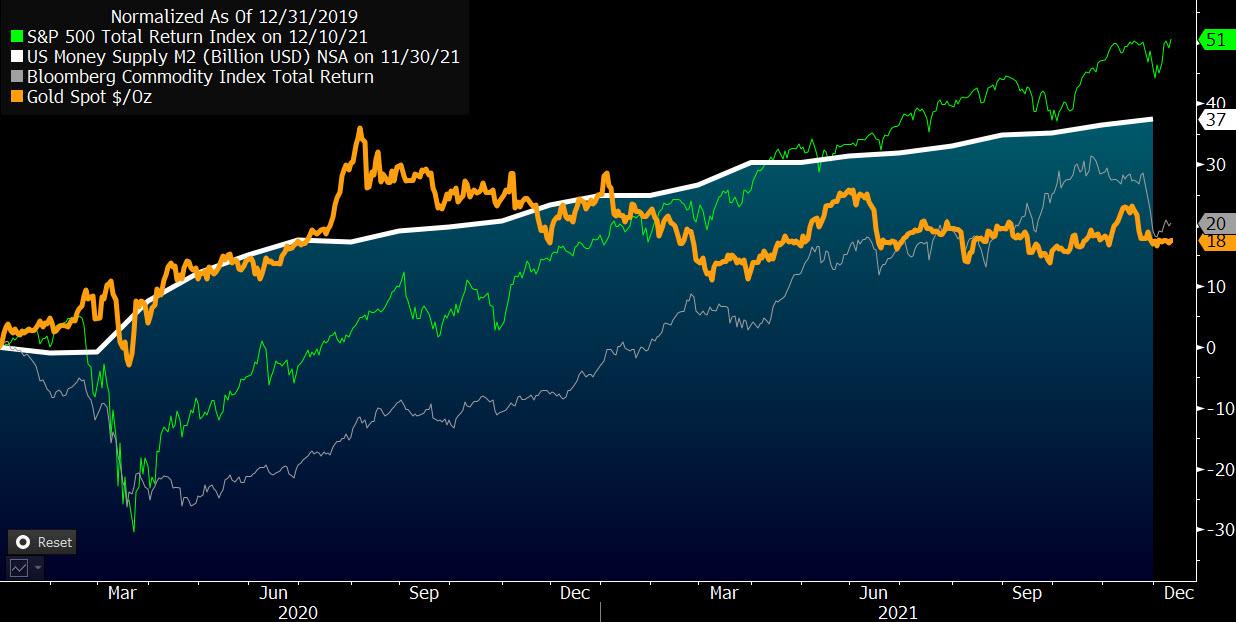

$100,000 BITCOIN, $50 OIL, $2,000 GOLD? 2022 OUTLOOK IN 5 CHARTS

By Mike McGlone, Bloomberg commodity strategist

Peaking commodities and the declining yield on the Treasury long bond point to risks of reviving deflationary forces in 2022, with positive ramifications on Bitcoin and gold. A primary uncertainty heading into the new year is whether the U.S. stock market can keep rising amid Federal Reserve restraint, with implications for all assets.

1. Money Supply Test: Sustainability vs. Vulnerability

Asset class performance in 2022 is likely to be all about the potential for reversion toward the upward trajectory of U.S. money supply, which should favor gold, especially if stock-market returns normalize some. What's different about that outlook, which has been relevant throughout much of history, is the proliferation of crypto assets. The fact that our graphic excludes the Bloomberg Galaxy Crypto Index (BGCI) due to distortions of its outsized performance, is a top reason cryptos are gaining exposure in portfolios.

So, will the trend turn, or are we in for more of the same? Our bias is the latter, notably because the BGCI has overcome about a 60% correction in 2021 vs. the S&P 500, which hasn't had a 10%-plus drawdown since the 2020 trough. Underperforming commodities face increasing pressure/

See Chart:

https://assets.zerohedge.com/s3fs-public/inline-images/vulnerability.jpg?itok=ao7HzGis

{kind=link}

3. Bitcoin Says: Why Complicate a Bull Market?

Bitcoin is a risk asset that's evolving into a digital reserve asset in a world going that way, with positive implications for its price. Demand and adoption are rising and still appear in early days vs. supply, which is declining. The key question nearing the end of 2021 is whether Bitcoin is too hot, and our chart shows the crypto fairly priced at about its upward-sloping 50-week moving average. Not too extended and within an upward trajectory sets the stage for a potentially strong 2022. Bitcoin ended 2020 around 140% above its annual mean.

The overextended condition a year ago has been relieved, and it's now a question of a consolidating bull or the beginning of a reversal. Our bias is with the former, on the back of favorable demand vs. supply fundamentals. About $100,000 is good target resistance.

See Chart:

https://assets.zerohedge.com/s3fs-public/inline-images/bitcoin%20weekly.jpg?itok=kIosfkbA

{kind=link}

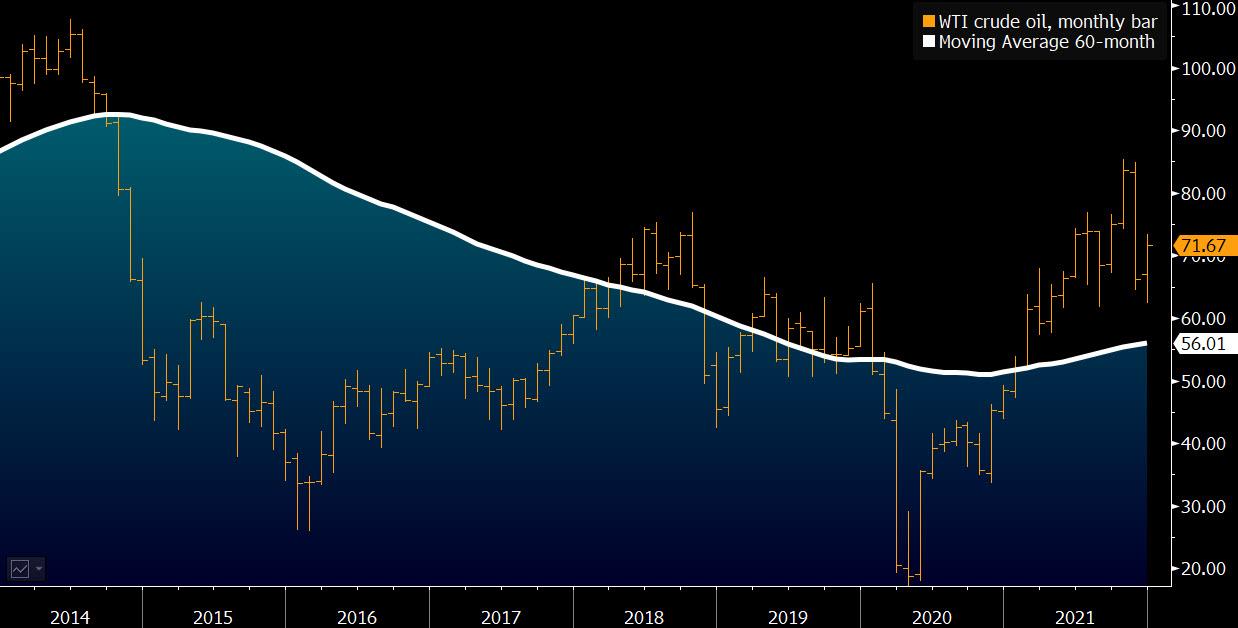

4. Crude Wonders: Why Complicate a Bear Market?

The big difference between commodities -- notably oil -- and Bitcoin is elasticity of supply, which points downward for crude prices in 2022. In 2021, West Texas Intermediate stretched the greatest distance above its 60-month moving average since the peak in 2008. This is a bad sign for prices. The price bounce is accelerating the paradigm shift of the U.S. gaining enduring status as a net crude and liquid-fuel exporter, and encouraging the proliferation of substitutes and electric vehicles.

We see unfavorable production vs. consumption, along with a challenging economic backdrop, and prices more likely to revert toward lower means. Our graphic depicts WTI appearing too hot at about $72 a barrel vs. its 60-month mean closer $56.

See Chart:

https://assets.zerohedge.com/s3fs-public/inline-images/WTI%20crude_0.jpg?itok=UYGR2x4m

{kind=link}

5. Alert to the Great Commodity Deflation

The risk of, and propensity for, some typical reversion in broad commodity prices may be a top development in 2022. Our graphic depicts the potential early days of normalization for the Bloomberg Commodity Spot Index following an almost uninterrupted rally from 2020's bottom. Commodity prices rising with China in decline is basically an oxymoron, based on historical patterns. The second cut of China's reserve requirement ratio in 2021 (and likelihood of more to come), running alongside declining yields on the U.S. Treasury long bond is a poor mix for higher prices.

China has been a primary source of demand for commodities, notably since 2003, and higher rates in the U.S. underpin the dollar, which typically is a headwind for commodity prices.

See Chart:

https://assets.zerohedge.com/s3fs-public/inline-images/china%20required.jpg?itok=GM0YjR59

{kind=link}

….

SOURCE: https://www.zerohedge.com/markets/100000-bitcoin-50-oil-2000-gold-2022-outlook-5-charts

----

----

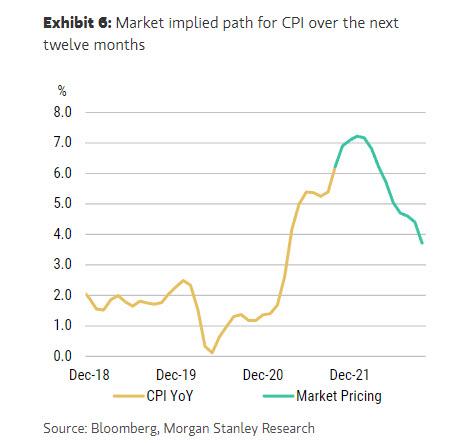

If Goldman is right, and the Fed is about to hike 7 times in the next three years, it is about to commit the biggest policy blunder of all time.

At the start of the month, not long after Goldman capitulated and brought forward its first Fed rate hike forecast by one year to July 2022, virtually every Wall Street bank promptly followed in Goldman's footsteps turning uber hawkish and expecting several rate hikes and/or accelerating tapering over the coming year. All, expect Morgan Stanley, which stubbornly refused to yield to peer pressure and continued to forecast no rate hikes in 2022 whatsoever.

This remarkable divergence in Fed outlooks between the two most influential banks promoted us to tweet on Dec 1 that "2022 shaping up as a huge showdown between Goldman and Morgan Stanley. Former says 2, maybe 3 hikes; latter say no hikes. One will be spectacularly wrong."

Just a few days later, with inflation soaring to a fresh 39-year-high (although perhaps finally topping out), Morgan Stanley decided to gracefully and quietly tap out and this week the bank's -chief US economist Ellen Zentner, pulled forward the bank's rate hike path by 6 months to September 2022, acknowledging that it was wrong and admitting that there has been a "pivot in the Fed's reaction function."

Even so, Morgan Stanley still remains well beyond market expectations, saying it has "even greater conviction" in its call that core inflation moves off its highs in 1Q 2022, which however further validates concerns that the Fed is engaging in a policy error and tightening into a recession.

Here are some more details from Zentner's note:

Before investors close out the year, we need to get past the FOMC's final meeting next week, and it comes with every opportunity for surprise. On Wednesday, we expect the Fed to move to a hawkish stance by announcing that it is doubling the pace of taper, highlighting continued inflation risks and no longer labeling high inflation as transitory, and showing a hawkish shift in the dot plot. We think this shift will shake out in a 2-hike median in 2022, followed by 3.5 hikes in 2023 and 3 hikes in 2024.

At the end of the meeting, we think the FOMC's median view will align more closely with ours – we look for 2 hikes in 2022, followed by 3 hikes plus a halt in reinvestments in 2023. Moreover, we expect the Fed's median forecast for core PCE and the unemployment rate will also come in reasonably close to our own, which now has higher inflation receding to around 2.5% 4Q/4Q next year, and the unemployment rate back to its pre-pandemic low around 3.5% in 4Q22. The incoming data on the labor market and inflation has strayed materially from the Fed's outlook and therefore warrants what we deem to be a sea change in its stance on the appropriate path for policy.

At the same time, Zentener also says that the timing of liftoff in the bank's forecast is tied closely to inflation outcomes, with its base case expectation that following the current re-acceleration in inflation we have been expecting, core PCE shows some slowing beginning in February next year. The pace of this deceleration will be important in determining how much of a breather the Fed takes between the end of its asset purchases and the first rate hike.

See Chart:

https://cms.zerohedge.com/s3/files/inline-images/market%20implied%20path.jpg?itok=ajTXbNvF

{kind=link}

In conclusion, Goldman's forecast calls for 3 hikes in 2022 (vs 2 for Morgan Stanley) and then 2 per year starting in 2023. The bank also expects two hikes per year starting in 2023 because like MS, it also expects inflation to fall to moderately above 2% and growth to slow to just above potential by then.

That said, Goldman's Jan Hatzius says that he "inferred from the September dots that Powell and Governor Brainard envision hiking twice per year in that environment, a slower pace than last cycle that we assume reflects the new monetary policy framework." However, the bank will watch the December dots to see if they still view that as the default pace.

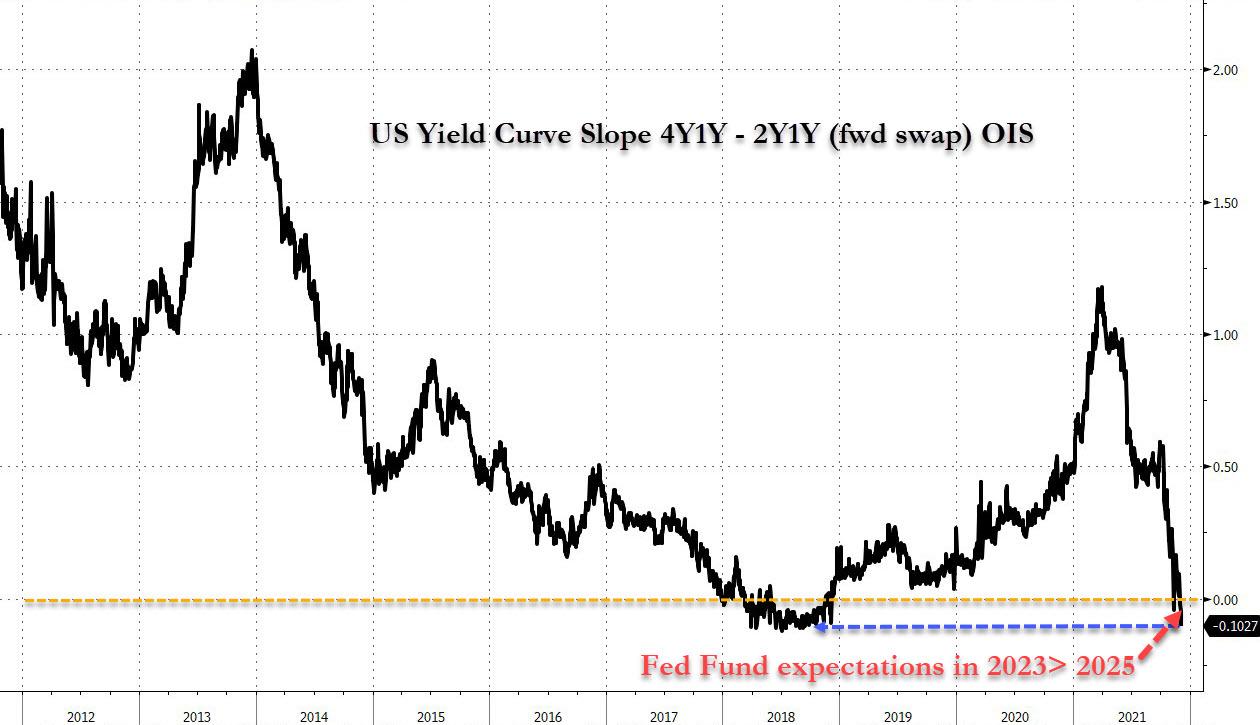

Or, one can just look at what the market is saying and the conclusion there is clear: with the 4Y1Y - 2Y1Y curve inverting...

See Chart:

US Yield Curve Slope 4Y1Y – 2Years 1 year (forward swap) OIS

https://cms.zerohedge.com/s3/files/inline-images/yield%20curve%20slope%20down_3.jpg?itok=Tciv8rWn

{kind=link}

... as STIR traders now expect rates in 2023 to be higher than in 2025, the verdict is simple: not only is the Fed engaging in policy error, hiking into an economic slowdown - with inflation having already peaked, someone has yet to explain to us how monetary policy will help alleviate supply chains, for example - but it will then proceed to rapidly cut rates (perhaps to negative) while injecting trillions more in QE once markets crash (amid the coming rate hike panic detailed meticulously by BofA CIO Michael Hartnett) to reflect the Fed's panicked actions (which an objective observer could say reek suspiciously of political pandering to appease Joe Biden who is clearly freaking out about his collapsing rating and the impact inflation is having on it) some time in late 2022, just before the midterms.

Read the full article at:

----

----

Morgan Stanley: As Uncomfortable As It Can Be To Admit Defeat, Here We Are

By Seth Carpenter, global chief economist at Morgan Stanley

Now the level, not just the trajectory of inflation, is key... and the Fed is set to accelerate the taper.

This past week, our US economics team revised its Fed call. The change is motivated by the notable shift in rhetoric from Chair Powell. I want to walk through some of the logic, some of the implications, and why we have not seen a second “taper tantrum.”

In November, the taper was announced. Since then, inflation prints have evidently surprised the Fed to the upside, and the public debate about inflation has reached fever pitch. A subtle, but to me particularly telling cue, was Chair Powell asserting that price stability is now the path to full employment. Waiting until 2Q or 3Q for inflation to fall is off the table. Now the level, not just the trajectory of inflation, is key...and the Fed is set to accelerate the taper.

A change in the reaction function means a change in our call. Of course, the market has been there for some time, and as uncomfortable as it can be to admit defeat, here we are. So what next?

In my time at the Fed, policy decisions were taken one step at a time. The faster taper – as Cleveland Fed President Mester noted –simply provides optionality, it does not commit the FOMC to a hike when it is done. In March, I suspect Chair Powell and team will want to pause to assess the markets and the economy. If our inflation call is right, they will have to wrestle with monthly inflation prints that are coming down faster than forecast.

Falling inflation should reduce, but not eliminate, the urgency to raise rates. Some persistence in trend inflation will remain, so we are looking for quarterly rate hikes, starting in September. Next, the question will be when to unwind the balance sheet. I was a debate participant inside the Fed during the last cycle. The winning argument was to start with rates because the Fed had experience with that tool but not with the balance sheet. One cycle using the new tool probably does not change the sequencing. Consider that the FOMC reversed course on rates in early 2019 while shrinking the balance sheet; tightening had gone too far, too fast. And in September that year, just months later, the Fed had to rebuild reserves after over-shrinking. A single cycle's worth of experience does not look like enough. Of course, now there is further to go, so the unwind may start a bit lower than the 1.25% level last time, but I suspect the playbook is largely unchanged.

Does a sea change at the Fed mean a tsunami for the rest of the world? In 2013, the 10-year yield troughed at 1.63% but ended the year a touch over 3%. Partly by design and partly by circumstance, we are in a different place today. Once bitten, twice shy: the Fed worked hard to avoid a taper tantrum this time. The foreshadowing started way back in the minutes of the September 2020 meeting.

Markets have started to price in Fed hikes, but yields have moved nothing like they did in 2013. Global inflation has already put many EM central banks on a hiking path; instead of being caught off guard, most have stayed ahead of the curve [ZH; just ignore China which is already in easing mode]. And even with the market pricing rate hikes, real US rates look likely to pick up only gradually. This time really does seem to be different.

….

SOURCE: https://www.zerohedge.com/markets/morgan-stanley-uncomfortable-it-can-be-admit-defeat-here-we-are

----

----

EL-ERIAN SAYS FED MADE "WORST INFLATION CALL EVER"

"It results in a high probability of a policy mistake."

====

US DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete; it’s full of frauds & corruption.

PANIC? US MEGA-CORPORATIONS RUSH TO ABANDON VAX MANDATE

Biden's mandates have always been a bullying gamble...

====

DHL IS KEEPING PACE WITH THE HOLIDAY RUSH BY ADDING 1,500 NEW ROBOTS

...on top of 15,000 seasonal staff.

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China, RU, Iran search for State socialis, D rest in limbo

G-7 WARNS RUSSIA OF "MASSIVE CONSEQUENCES" FOR UKRAINE INCURSION

"...we are considering all options,”

====

SPUTNIK NEWS : https://sputniknews.com/

- Swedish Greens Reported for Inciting Ethnic Hatred After Blaming Russia for High Electricity Prices

- BoJo Won't Resign in Short-Term, But His Political Future Teetering

- South Korea Not Considering Boycott of Beijing Winter Olympic Games

- US President Biden Approves Kentucky Disaster Declaration

- Pelosi Reportedly Intends to Lead House Democrats Through 2022 Midterm Election

- New Potential Crisis Arising From NATO Buildup on Russian Border Hard to Predict

- Omicron Strain Could Reduce Effectiveness of Pfizer Shots by More Than 30 Times

- Rosneft Expects Russian Government to Give Company Access to Gas Exports

- Assange’s Fiancee Accuses US of Using UK as ‘Executioner’ in Plot to Kill WikiLeaks Founder

====

====

DIC 12 2021 PART 2 ND SIT EC y POL SPANISH ++

US: Joe Biden y la violación de la democracia Marc Vandepitte

Alem: nuevo Go de Alemania es esclavo de los halcones neoliberales

Ecol S: Semillas para los pueblos, campaña global contra priva UPOV

ARG: Los imprecisos y siempre espeluznantes efectos del default

BRA: LA TERCERA VÍA: CABALLO DE TROYA Boaventura de Sousa S

Opin: Periodismo clandestino en territorios ocup del Sáhara Occid

Opin: Cuando despertó, el proletariado todavía estaba allí M M

MX: LA NOVEDAD DEL GRUPO DE PUEBLA Pedro Brieger

España: FERROCARRIL, EFICIENCIA Y CAMBIO CLIMÁTICO P L A

España: EL MURO Y LA MUGA Iñaki Egaña

Marruecos La guerra crea más represión sobre civiles saharauis

Djibril Diallo: Unidad y lucha contra discr de África y su diáspora

----

----

RT EN ESPAÑOL

Rusia advierte sobre "duras consecuencias" si la OTAN se expande https://actualidad.rt.com/actualidad/413435-rusia-otan-expansion

….

Putin: si ellos tienen armas hipersónicas, es posible que RU tenga como eliminarlas https://actualidad.rt.com/actualidad/413416-putin-socios-armas-hipersonicas-medios-eliminar

….

Alemania advierte que todavía no autorizará el gasoducto Nord Stream 2 de RU https://actualidad.rt.com/actualidad/413437-alemania-advierte-autorizara-gasoducto-nord

….

Moscú denuncia que Occidente continúa la militarización de Ucrania https://actualidad.rt.com/actualidad/413436-moscu-denuncia-occidente-continua-militarizacion-ucrania

….

Omicron: "Parece que estuvo escondida durante un año" https://actualidad.rt.com/actualidad/413377-desata-polemica-cientificos-origen-cepa

….

Duras críticas a decisión d la Justicia británica de autorizar extrad de Assange a US https://actualidad.rt.com/video/413419-duras-criticas-decision-justicia-britanica-extradicion-assange-eeuu

….

US destina 20 mills de dólares para que Ucrania responda a Rusia y Bielorrusia https://actualidad.rt.com/video/413356-eeuu-destinara-20-millones-dolares-ucrania

….

….

GLOBAL RESEARCH

Geopolitics & Econ-Pol crisis that leads to more business-wars from US-NATO allies

- Climate Famine in Afghanistan By Jonathan Neale

- 57 Top Scientists and Doctors Release Shocking Study on COVID Vaccines and Demand Immediate Stop to All Vaccinations By Dr. Roxana Bruno

- The “Vaccine” and “The Great Reset”: Archbishop Carlo Maria Vigano Points to Crimes against Humanity By His Excellency Carlo Maria Viganò

- The “Killer Vaccine” Worldwide. 7.9 Billion People By Prof Michel Chossudovsky

- Joe Biden and the Rape of Democracy. Cold War Rhetoric. Obedience to the US By Marc Vandepitte

- Assange and Reversal in the UK High Court. The Extradition Procedure By Dr. Binoy Kampmark

====

====

No hay comentarios:

Publicar un comentario