Aug 26 2021 ND SIT EC y POL Part 1

ND denounce-neoliberal debacle y propone State-Social + Capit-compet in Eco

ZERO HEDGE ECONOMICS

Neoliberal globalization is over. Financiers know it, they documented with graphics

DOWN!

STOCKS SLUMP ON KABUL BLAST, KAPLAN BANTER, & CRAPPY DATA

by Tyler Durden

It appears the short-squeeze is over...

Dip-buyers still kept charging in during the day - terrible news is great news for markets right!? WTF is wrong with us.

Stocks did get real into the last hour as The Pentagon laid out the grisly details of what had occurred. Small Caps were hardest hit all the majors ended the day down hard...

See Chart:

https://cms.zerohedge.com/s3/files/inline-images/2021-08-26_13-00-02.jpg?itok=KDXZPWqn

{kind=link}

It appears the short-squeeze is over as "Most Shorted" stocks - despite yet another attempt at the open, and at the European close to stage a ramp - ended lower on the day...

See Chart:

Most Shorted Stocks

https://cms.zerohedge.com/s3/files/inline-images/bfmC69.jpg?itok=alsEc4_K

{kind=link}

Short-term VIX spike dramatically relative to far-term VIX after a week of confident compression into tomorrow's J-Hole speech...

See Chat:

https://cms.zerohedge.com/s3/files/inline-images/bfm64AB.jpg?itok=tsCa1dsZ

{kind=link}

Treasury yields roller-coastered on the day, but ended mixed with the long-end outperforming (30Y -1bps, 5Y +2bps) ahead of tomorrow's likely vol-splosion from Powell...

See Chart:

https://cms.zerohedge.com/s3/files/inline-images/bfmF162_0.jpg?itok=QKPc3uXc

{kind=link}

The dollar rallied off support once again today...

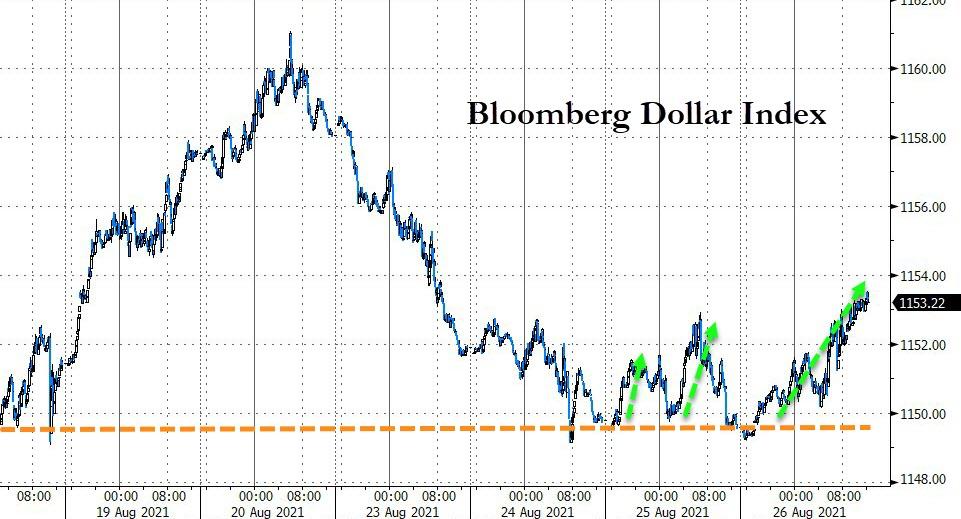

See Chart:

Bloomberg Dollar Index

https://cms.zerohedge.com/s3/files/inline-images/bfmC15E.jpg?itok=4sQ8vhGj

{kind=link}

Gold rallied up to $1800 intraday but faded back, but did end higher on the day...

See Chart:

https://cms.zerohedge.com/s3/files/inline-images/2021-08-26_12-14-03.jpg?itok=fGW-GayH

{kind=link}

Oil prices were very choppy today - war premium or no war premium? - with WTI testing down towards $67...

See Chart:

https://cms.zerohedge.com/s3/files/inline-images/2021-08-26_12-15-20.jpg?itok=P41gZfYA

{kind=link}

Finally, as the world and their pet rabbit contemplate Powell's words tomorrow and whether ending The Fed's balance sheet expansion should be done sooner than later, consider that maybe, just maybe QE ain't f**king doing anything for the real economy...

See Chart:

https://cms.zerohedge.com/s3/files/inline-images/bfmFEAB_0.jpg?itok=ykseP9kP

{kind=link}

But then again, what does that matter? All that appears to be on the minds of this new generation is stimmies in ma pocket and record highs for stonks...

See Chart:

Fed Balance Sheet vs S&P 500

https://cms.zerohedge.com/s3/files/inline-images/bfm4023_0.jpg?itok=mRrWopJC

{kind=link}

THIS WILL NOT END WELL!

….

SOURCE: https://www.zerohedge.com/markets/stocks-slide-kabul-blast-kaplan-bullard-bad-data

----

----

PETER SCHIFF BLASTS JEROME POWELL'S "BAD ECONOMICS"

"...what the government did is try to pretend that nobody actually had to suffer because the government can make everybody’s pain go away simply by printing money. Well, they didn’t make the pain go away. They

====

BANK OF AMERICA'S TOP FEMALE EXECUTIVE ANNOUNCES RETIREMENT

Just after a woman took over a Wall Street megabank for the first time, one of BofA's top female executives is heading for the exit.

----

----

LABOR SHORTAGES: "WE MAY BE CLOSER TO THE BRICK WALL THAN ANTICIPATED"

By Philip Marey, senior US strategist at Rabobank

As the temporary labor shortages disappear and the permanent labor shortages become visible, the Fed may find there is less slack in the labor market than anticipated. Consequently, the Fed may have to make an

Labor shortages: temporary or permanent?

Summary

· While Republicans and Democrats are pointing to different causes for the temporary labor shortages, the empirical evidence suggests that both unemployment benefits and child care considerations are playing a role. However, these temporary effects should fade during the course of September.

· More importantly, a permanent labor shortage is caused by retirement. This means that we should not expect a recovery of the participation rate to pre-COVID levels.

· As the temporary labor shortages disappear and the permanent labor shortages become visible, the Fed may find there is less slack in the labor market than anticipated. Consequently, the Fed may have to make an additional upward shift in the dot plot in the coming months.

Introduction

Although employment is still well below pre-COVID levels (about 5.7 million in July, Figure 1), employers are having a difficult time filling their vacancies. The ratio of unemployed persons to job openings, a measure of labor market looseness, fell to 0.94 in June, comparable to levels in 2018 (Figure 2), when the Fed accelerated the hiking cycle to four hikes in one year, because it mistakenly saw high inflation around the corner This paradox, a shortfall in employment and an apparent labor shortage, has been attributed to a number of factors causing a temporary labor shortage. Three main causes are often being mentioned: the enhanced federal unemployment benefits from the American Rescue Plan, fear of COVID, and lack of child care.

See Charts:

1: Shortfall in employment. 2: And a tight labor market

https://cms.zerohedge.com/s3/files/inline-images/shortfall%20employment.jpg?itok=Ixwt7DWl

{kind=link}

View from the right: Unemployment benefits

As we shift to the left side of the political spectrum, fear of COVID and lack of child care are increasingly given as explanations for the current labor bottlenecks. As we have pointed out earlier, the Democrats want to make the child tax credit enhancements in the American Rescue Plan permanent. However, their claim seems to be supported by the data. First of all, up to a third of the US workforce has children aged 14 or younger in the household (Dingel et al. 2020). This means that the reopening of schools and daycare centers could be an important bottleneck for labor supply. Especially, the participation of women in the labor market could be severely affected. In fact, there is empirical evidence (Lofton et al., 2020) that the labor supply of mothers was less depressed in states that reported less disruption to schooling. Meanwhile, it appears that businesses are reopening at a faster pace than schools. By the end of this past school year, only 53% of schools had fully reopened for in-person instruction (Ferren, 2021).

Taking the views from the right and the left together, there is empirical evidence there is a temporary labor shortage caused by the phase of the COVID crisis and fiscal policy. Consequently, once COVID subsides, schools have reopened and enhanced federal benefits have expired, labor supply is likely to rebound and we should be back to an overall looser labor market, apart from scarcity in certain specific occupations.

Structural decline in participation?

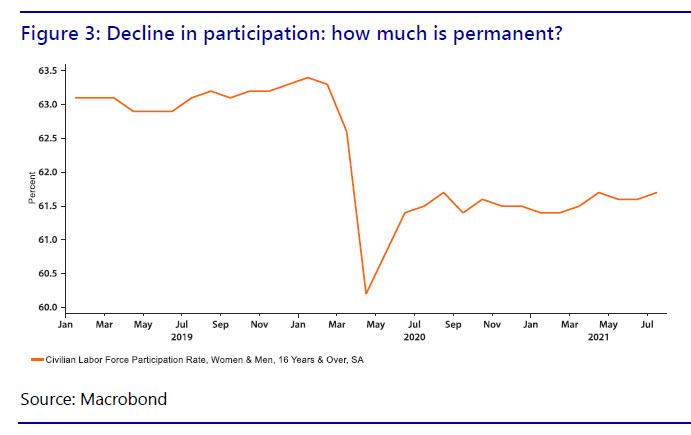

However, while part of the decline in labor participation (Figure 3) can be explained by child care considerations, fear of COVID and enhanced unemployment benefits, there is also a more permanent factor reducing participation: retirement. According to calculations made by the Dallas Fed (Kaplan et al. 2021) a few months ago, in addition to 4.1 million joining the unemployed since February 2020 there were 4.4 million not currently actively looking for work: 1.3 million because of caregiving and 2.6 million because of retirement. The caregivers may largely return when schools reopen, but how many retirees will return to the labor market? After all, it appears that many already delayed retirement during the tight labor market of 2018-2019. These figures suggest that retirement is playing a larger role than child care, which also means that the permanent decline in participation may be larger than many are now thinking.

See Chart:

Decline in participation: how much is permanent?

https://cms.zerohedge.com/s3/files/inline-images/decline%20in%20participation.jpg?itok=zW88_Via

{kind=link}

False sense of slack

This also means that adjusting unemployment rates for lost participation is misleading. For example, Powell (February 10, 2021) has been referring to an alternative unemployment rate - based on the pre-COVID19 participation rate - being much higher than the official unemployment rate. This measure would suggest that there is still a lot of slack in the labor market. However, if a substantial fraction of the labor force outflow is not going to come back, slack is actually much smaller than suggested by a fixed participation unemployment rate. Looking at this measure will give the FOMC a false sense of slack that could cause the Committee to react too slowly to a tightening labor market.

Conclusion

Next month should be crucial for the labor market as temporary labor shortages are expected to disappear, and more permanent labor shortages will become visible.

For the Fed a temporary labor shortage means that upcoming monetary policy decisions – such as giving signals about tapering – will have to be made in a noisy environment where data are being distorted. We called this the “data fog” in Early Warning Signal in a Noisy Environment. Employment growth is temporarily slowed down, but should accelerate once the causes of the temporary labor shortage fade.

However, once we come out of the data fog, we may be closer to the brick wall than anticipated. If there is also a permanent component to the decline in labor participation, then slack in the labor market is smaller than suggested by the downdraft in the employment level (Figure 1). For the FOMC, the smaller the shortfall in employment the earlier they may want to hike. The higher-than-expected inflation readings in recent months have already led to an upward shift in the dot plot, indicating that the FOMC now expects to hike twice in 2023, instead of waiting until 2024. If more of the “temporary” labor shortage turns out to be permanent, the FOMC may be forced to shift its first hike to 2022.

….

SOURCE: https://www.zerohedge.com/economics/labor-shortages-we-may-be-closer-brick-wall-anticipated

----

----

US DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete; it’s full of frauds & corruption.

Biden has ‘mental lapsus’: he need a psychiatric asap

BIDEN DELIVERS SURREAL PRESS CONFERENCE, VOWS TO HUNT DOWN ISIS, BLAMES TRUMP

"I have another meeting, for real..."

====

“Basically, they just put all those Afghans on a kill list. It’s just appalling and shocking and makes you feel unclean.”

====

"...While It's rare - it's certainly not isolated...One hospital has had well over a dozen cases like me."

====

Is anyone sick of being ruled and owned yet?

====

THE ALL-SEEING "I": APPLE JUST DECLARED WAR ON YOUR PRIVACY

Snowden opines...

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China, RU, Iran search for State socialis, D rest in limbo

"Almost a certainty..."

====

NEW REPORT FINDS US HAS SPENT OVER $2.3 TRILLION ON AFGHANISTAN WAR

Brown University’s Costs of War project just updated

its long-running study this week...

====

"Canada is nothing but a tool for the United States to exploit, suppress dissidents, and seek personal gain. There is no fairness and legitimacy..."

====

BEIJING CLAIMS ITS PLANS TO "REDISTRIBUTE WEALTH" WON'T INVOLVE "KILLING THE RICH"

Those who "get rich first" should help those behind...but we must also "guard against the trap of welfarism".

====

SPUTNIK NEWS : https://sputniknews.com/

The Circus got a good Clown

-'We Will Not Forgive, We Will Not Forget': Biden Vows to Hunt Down Terrorists Behind Kabul Blasts

- US Supreme Court Lifts Federal Eviction Moratorium

- Angela Merkel Leads as The Most Supported Politician Among All World Leaders

- Video: Footage Appears to Capture Taliban Militants Maneuvering Black Hawk Chopper

- Real Madrid Raises Stakes, Proposing €180 Million to PSG's Kylian Mbappé

- Afghanistan Debacle May Threaten Biden's Chances For Second Term

====

====

No hay comentarios:

Publicar un comentario