WHY MASSIVE N. of YOUNG ADULTS

LIVING AT HOME WITH PARENTS

Millennials are living at home for the following reasons:

-Heavy levels of student debt

-Lower wages

-Inability to afford current home prices and in many markets, current

rents

INTRODUCTION by Tyler

Durden on 12/14/2014

The Federal Reserve conducted a study on Millennials and

tried to ascertain why so many of them are living at home. Is it too much

student debt? Lower incomes? Or is it that home prices are simply

unaffordable? The study finds that all of these factors have a big impact

on why many Millennials are living at home and why the first time home buyer

market is performing so badly.

Via Dr. Housing Bubble blog, http://www.zerohedge.com/news/2014-12-14/why-milennials-are-stuck-living-home-parents

The Federal Reserve conducted a study on Millennials and

tried to ascertain why so many of them are living at home. Is it too much

student debt? Lower incomes? Or is it that home prices are simply

unaffordable? The study finds that all of these factors have a big impact

on why many Millennials are living at home and why the first time home buyer

market is performing so badly. It also gives us insight into the shifting

building demand of new construction. Many builders are focusing their energies

on multi-unit structures to cater to an audience that will look for rentals or

lower priced condos. There is a heavy

renting trend undertaking this country. We are seeing a record numbers of

young people living at home with mom and dad heading directly back into their

childhood rooms to rock out the NES and attempting to pass Super Mario Brothers

once again. There are major implications for housing because of this new

structural change. First time home buying is down dramatically. Construction is

catering to a lower income cohort. Let us look at what the Fed found in their

report.

The massive number of young

adults living at home

One of the interesting findings

is that the trend of young adults living at home has continued on an upward

slope going all the way back to 1999. Even the toxic mortgage days of Housing

Bubble 1.0 didn’t really shift this figure by much. But the homeownership rate

increased which means that the push came from older cohorts or young buyers

that had the misfortune of buying near the top (and of course many were burned

in epic fashion).

So let us look at the findings:

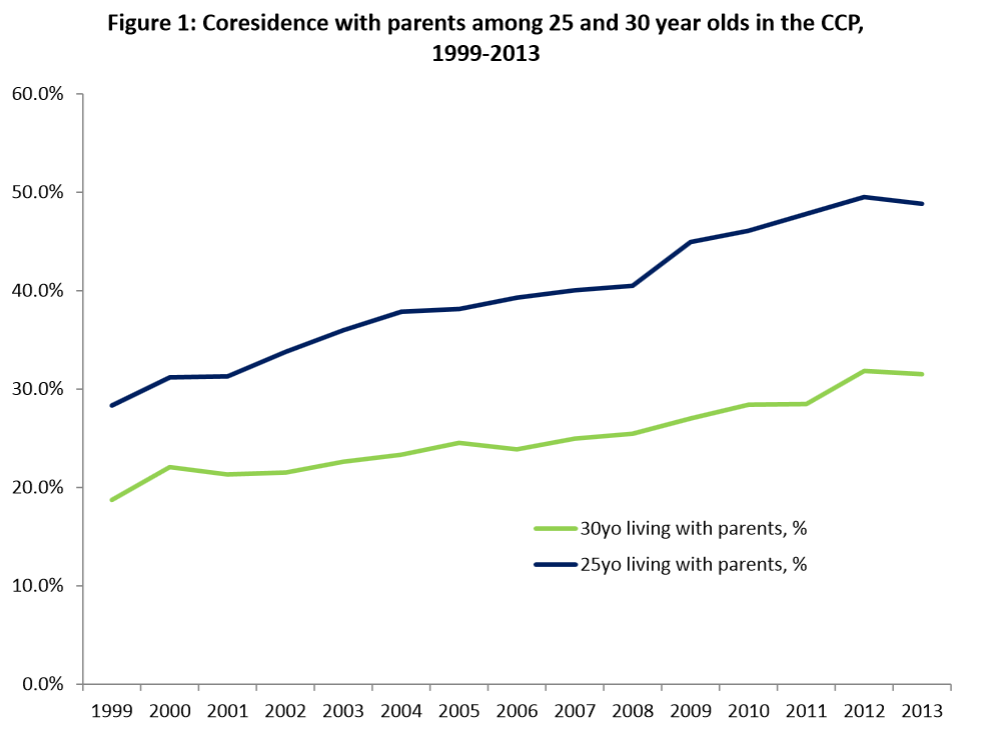

Nearly half of those 25 years of age are living at home

with parents. The rate is up to 30 percent for those 30 years of age. These

are dramatic increases from 1999. There has been paltry data on the makeup of

housing composition because some were saying that many were shacking up with

roommates. That does not appear to be the case:

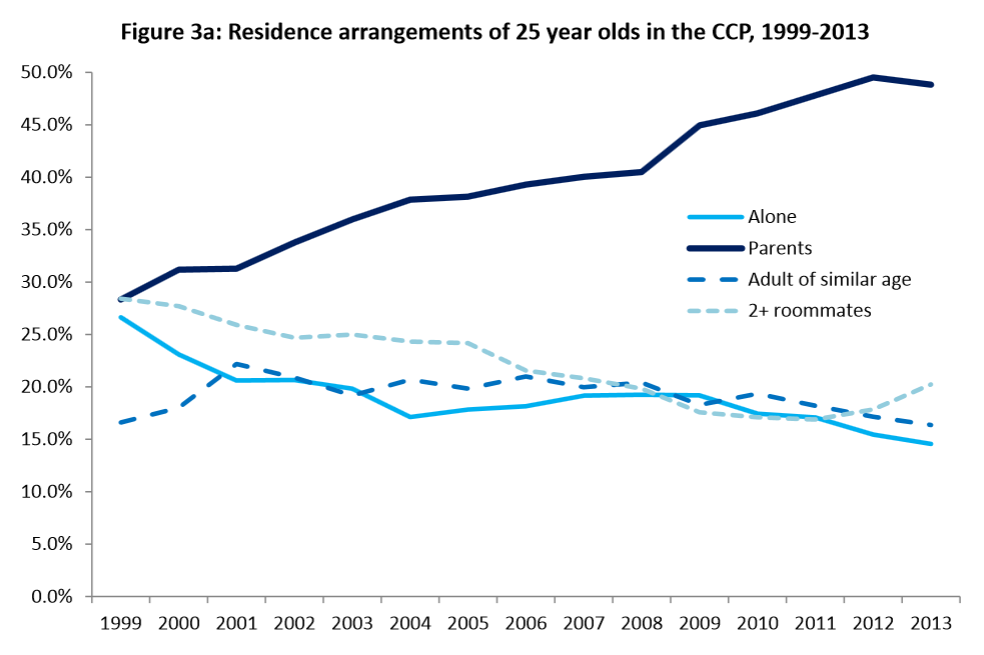

If you were placing a bet, you would be in a good

position putting your money on those 25 years of age living at home with

parents. The first time home buyer market continues to perform

pathetically. Of course, with investors pulling back we now have the FHFA

trying to push for 3 percent down payment loans to get the juices flowing

again. We are already at 5 percent down payments so this move to 3 percent will

likely offer minimal help for younger Americans.

One of the better graphs from the Fed report is the

combination of all these factors into one spot:

That is Figure 7 skipped (too big)

The homeownership rate of the 30 year old cohort has

tanked starting in 2007 with the market implosion. That is very clearly

illustrated by the green line above. Why? These were the folks buying with

toxic mortgages and timed the market very poorly (or simply had bad luck). The

rate of those young adults living at home has gone up unabated since 1999. Of

course the increase in home prices has been driven

by investors and this will simply make it harder on a cohort with lower

incomes and much higher levels of student debt.

It is safe to say that many more young Americans will

be renting

deep into their adulthood. It is also safe to say given the current cost of

college that many more young Americans will be coming back home to live with

mom and dad. The Fed’s findings are simply reinforcing this trend.

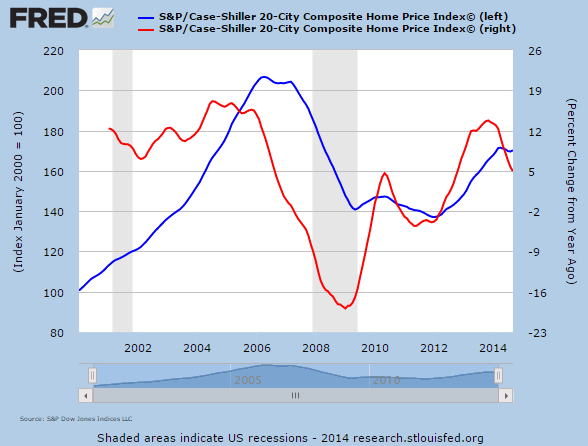

Given the boom and bust nature of housing, we already see

that the rate of price increases is slowing down very quickly:

The pattern seems to be clear. Prices ramp up. The economy

hits a hiccup. And prices come trending lower. This even happened in the 2010

to 2012 period. Look at where we are at right now. And the recent run up in

2013 was largely driven by a fickle group in investors.

Millennials are living at home for the following reasons:

-Heavy levels of student debt

-Lower wages

-Inability to afford current home prices and in many markets, current

rents

So how this sets up for a pent up demand for expensive

homes or nicely painted

crap shacks is really beyond the data.

The demand will be from older Friskie eating

households, investors, and foreign buyers.

* * *

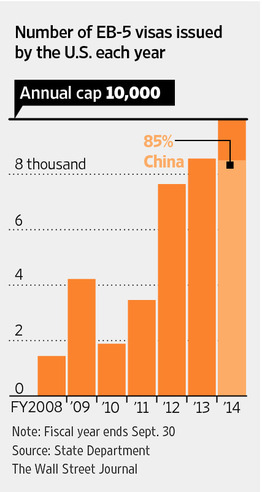

It was interesting to see the number of EB-5 visas being pumped out largely to those from China:

“(WSJ)

To finance the concrete-steel platform, Related tapped a little-known and at

times controversial federal visa program known as EB-5, which offers green

cards to foreign families who invest at least $500,000 in U.S. projects that

create at least 10 jobs per investor.”

It doesn’t even have to be 10 jobs necessarily but the

hours have to work-out to the equivalent of 10 jobs. I’ve heard of people buying

places like yogurt stores or fast food chains. Not exactly 10 great paying jobs

but enough to keep young adults living at home with mom and dad. Since real

estate volume is low margin in some markets, even having a few hundred buyers

in one area can shift prices dramatically:

“(WSJ) These investors aren’t coming for the investment,” said Yi Song, a New York lawyer who works with Chinese clients. “They are coming here for their children to obtain a better education and to get residence as an insurance policy.”

The EB-5 program was virtually non-existent in terms

of volume even just a few years ago. That is no longer the case.

But again, the demand isn’t coming from younger Americans

that are suddenly making so much money that they are buying real estate. Short

of better paying jobs, the first time buyer market is going to have a tough

time.

====

RELATED ARTICLES:

-----

-----

-----

-----

-----

=====

No hay comentarios:

Publicar un comentario