JAN 6 2022 Part 1-2 SIT ECON y POL

ND denounce-neoliberal debacle y propone State-Social + Capit-compet in Eco

ZERO HEDGE ECONOMICS

Neoliberal globalization is over. Financiers know it, they documented with graphics

Quick News

HOW TO INVEST WHEN THERE'S NOWHERE TO HIDE

Stocks, bonds, real estate, cash all look set to lose value.

====

Health:

JUDGE REJECTS FDA'S 75 YEAR DELAY ON VAX DATA, CUTS TO JUST 8 MONTHS

by Tyler Durden

"This is a great win for transparency..."

A federal judge has rejected a request by the FDA to produce just 500 pages per month of the data submitted by Pfizer to license its Covid-19 vaccine - and has ordered them to produce 55,000 pages per month. Assuming there are roughly 450,000 pages, that means it will take just over eight months for the world to see what's under the hood.

Boom! Very bad for a certain company. $PFE

See Chart:

I am pleased to report a federal judge rejected the FDA's request to produce the Pfizer Covid vaccine data at 500 pages per month and instead ordered a rate of 55,000 pages per month! Everyone should read the Judge's excellent 3-page decision available at

….

SOURCE: https://www.zerohedge.com/covid-19/judge-rejects-fdas-75-year-delay-vax-data-cuts-8-months

----

----

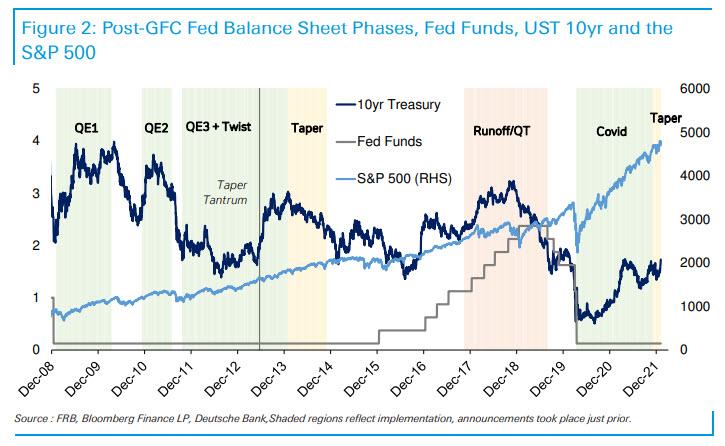

A TALE OF TWO QTS or Quantitative Tightening,

by Tyler Durden

When we get QT in 2022, Reid asks

"will it be more like 1999/2000 or 2018/2019?"

Yesterday’s FOMC minutes confirmed that the Fed is serious about launch an early runoff of their massive, nearly-$9 trillion balance sheet. It reminded DB's Jim Reid of two very different tales of Fed liquidity reversals over the last 25 years.

First, there are those who suggest that the last stage of the equity bubble of 1999/2000 and subsequent crash was encouraged by the Fed being petrified by the unknowns of the Y2K. They pumped in a huge amount of liquidity into the financial system in Q4 1999 which saw a big increase in the money supply and the Fed balance sheet, as shown below.

See Chart:

{kind=link}

In some ways, Reid writes, the increase in the Fed balance sheet from around $570bn to $670bn in Q4 1999 seems quite quaint relative to what we saw post GFC and during Covid. This brings us to the modern day QT, or quantitative tightening, when in October 2017 the Fed started to reduce its balance sheet from around $4.47tn to a low of around $3.76tn at the end of August 2019, at which point a mini freakout and repo crisis took place when markets realized that there was not nearly enough reserves in the system to assure smooth operations for levered financial institutions like hedge funds and commercial banks.

QT from 2017-2019 hardly had any impact on equities overall as can be seen in the second chart but there was a large sell-off in Q4 2018 when Powell commented that rates are a "long way" away from neutral which sparked panic that much more hiking was in stock, until Powell sharply pivoted on continued Fed hikes in January 2019. So, QT and hikes certainly interrupted the long equity bull market. For bonds, they initially sold off during QT but rallied hard in the second half of QT, mainly from when the equity market sold off in Q4 2018, and continuing after the Powell dovish pivot.

See Chart:

https://cms.zerohedge.com/s3/files/inline-images/post%20GFC.jpg?itok=ypGu-F0t

{kind=link}

So, when we get QT in 2022, Reid asks "will it be more like 1999/2000 or 2018/2019?" Both were tough for markets but on a very different scale. We now have US equity valuations that are only rivalled in history by what we saw in 1999/2000. However, before we get too excited, liquidity is still very high and, as we saw in 2018/2019, it took a year of QT and a series of rate hikes to create major market problems.

Regardless, as Reid concludes, "it seems that the age of ultra, uber, ludicrously loose monetary policy is coming to an end. It's inevitable markets will be impacted" while the timing is more debatable. And while markets may be quick to react, the economic problems of tighter policy probably won't be fully felt for a couple of years, at which point the Fed will likely proceed with the biggest easing cycle in history.

….

SOURCE: https://www.zerohedge.com/markets/tale-two-qts

----

----

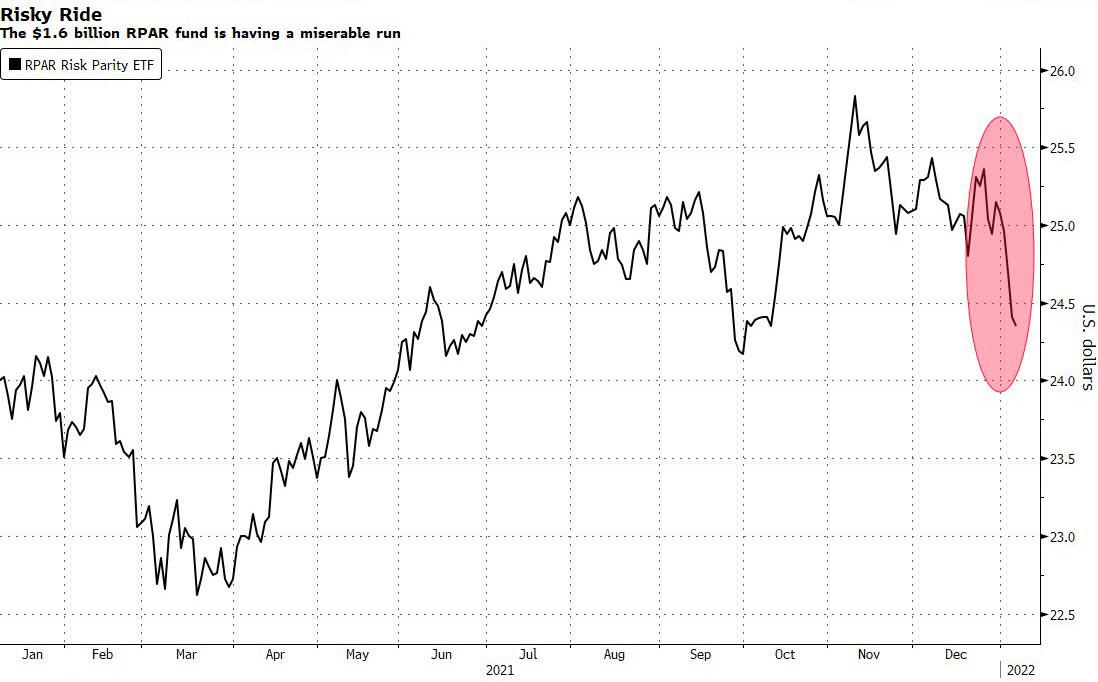

RISK PARITY ETF SUFFERS BIGGEST DROP SINCE COVID CRASH

by Tyler Durden

"It could be worse, you could be running a risk-parity fund"

While secretive risk-parity hedge funds such as Bridgewater will reveal their losses from the recent market turmoil in due time, there is one investment vehicle which invests in portfolios of stocks and bonds and which reveals in real time just how much pain its has suffered as a result of the concurrent plunge in equities and Treasuries in recent days.

The $1.6 billion RPAR Risk Parity exchange-traded fund (ticker RPAR) - the biggest of its kind - has dropped 3.4% in the five trading days through Thursday, on course for the worst five-day streak since March 2020. Its systematic strategy, popularized by Bridgewater’s Ray Dalio, allocates across asset classes based on risk and tends to suffer outsize losses when markets fall together.

See Chart:

Risky Ride: The 1.6 billion RPAR fund is having a miserable run

https://cms.zerohedge.com/s3/files/inline-images/rpar%20etf.jpg?itok=voUBOZFZ

{kind=link}

According to Bloomberg, the cross-asset volatility is also bad timing for RPAR’s new sister fund launched this week, which seeks to amp up returns with extra leverage (yes, that's leverage upon leverage). The RPAR Ultra Risk Parity ETF (UPAR) has fallen in each of its first three trading days, including a 1.5% slump on Wednesday -- a drop that equals some of RPAR’s worst moves in the past year.

Both funds traded lower on Thursday in New York as the S&P 500 fluctuated and Treasuries extended their retreat.

While risk-parity indexes hit records in 2021 as reopening optimism fueled stocks and commodities while dovish central banks kept bond yields in check, runaway inflation and the Fed's hiking intentions are disrupting the “everything rally” and making life for balanced portfolio investors miserable.

Worse, since risk parity funds target a level of risk by allocating across assets based on their volatility and then levering up, that means that during times of market turbulence they can be forced to unwind positions exacerbating price moves. That's what happened during March 2020 when Treasury yields first exploded then crashed.

RPAR and its levered cousing, UPAR, are actively managed but seek to match the returns of an index across four major asset classes: global equities, commodities, Treasuries and Treasury Inflation-Protected Securities, or TIPS.

….

SOURCE: https://www.zerohedge.com/markets/risk-parity-etf-suffers-biggest-drop-covid-crash

----

----

SHIFT TO QUALITY INTENSIFIES THANKS TO HAWKISH FED

By Ishika Mookerjee, Bloomberg Markets Live commentator and analyst

“Asian quality stocks tend to outperform during global slowdown, inflationary regime in Asia and in the following 12 months post China slowdown."

Demand for quality stocks is strengthening in Asia as the Federal Reserve dials up its hawkish commentary, making riskier firms look more vulnerable with borrowing costs expected to rise.

The MSCI AC Asia ex-Japan Quality Index has climbed about 1% since the end of October as the Fed announced its plan to taper asset purchases, while the MSCI AC Asia ex Japan Index has slumped 4%. The gauge of stocks with a high return on equity, stable earnings growth and low leverage trounced the broader benchmark by about nine percentage points last year, a better relative performance than that seen in its global peer.

See Chart:

Quality lasts

https://cms.zerohedge.com/s3/files/inline-images/quality%20lasts%20msci%20asia.jpg?itok=1iwu6NIz

{kind=link}

“Asian quality stocks tend to outperform during global slowdown, inflationary regime in Asia and in the following 12 months post China slowdown,” There’s also support from positive earnings revisions and a historical discount to low-quality stocks, they added.

Investors are dumping riskier companies, yet the outperformance of the quality gauge suggests they are still comfortable betting on the more mature tech companies in the region. The sector had the biggest weighting in the gauge as of November with software firms Infosys and Tata Consultancy Services as well as chip giant Taiwan Semiconductor Manufacturing among the largest constituents. Their shares are up 9%, 12% and 9% respectively since the end of October, despite pressure on the global tech sector

While the jury’s still out on China’s internet behemoths, semiconductor stocks are expected to fare better in Asia amid an ongoing chip shortage. The 12-month forward earnings estimates for Samsung Electronics and TSMC have risen more than 20% in the past year and over 50% for SK Hynix. That’s while the MSCI Asia Pacific Communication Services Index -- which includes Tencent -- saw a drop of 13% in its earnings estimates.

Given inflationary pressures, high-yielding quality stocks in Taiwan and China are preferred by Bernstein. “We are most bullish on staples, tech and energy while being most negative towards discretionary and industrials,” the analysts wrote.

The median forecast in Bloomberg’s survey of analysts anticipates the FOMC will raise its policy rate twice this year and three times next.

….

SOURCE: https://www.zerohedge.com/markets/shift-quality-intensifies-thanks-hawkish-fed

----

----

SHIFT TO QUALITY INTENSIFIES THANKS TO HAWKISH FED

By Ishika Mookerjee, Bloomberg Markets Live commentator and analyst

“Asian quality stocks tend to outperform during global slowdown, inflationary regime in Asia and in the following 12 months post China slowdown."

Demand for quality stocks is strengthening in Asia as the Federal Reserve dials up its hawkish commentary, making riskier firms look more vulnerable with borrowing costs expected to rise.

The MSCI AC Asia ex-Japan Quality Index has climbed about 1% since the end of October as the Fed announced its plan to taper asset purchases, while the MSCI AC Asia ex Japan Index has slumped 4%. The gauge of stocks with a high return on equity, stable earnings growth and low leverage trounced the broader benchmark by about nine percentage points last year, a better relative performance than that seen in its global peer.

Given inflationary pressures, high-yielding quality stocks in Taiwan and China are preferred by Bernstein. “We are most bullish on staples, tech and energy while being most negative towards discretionary and industrials,” the analysts wrote.

The median forecast in Bloomberg’s survey of analysts anticipates the FOMC will raise its policy rate twice this year and three times next.

….

SOURCE: https://www.zerohedge.com/markets/shift-quality-intensifies-thanks-hawkish-fed

----

----

US DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete; it’s full of frauds & corruption.

US Democ was destroyed by Big Corp who finance Electoral Politics of both R & D

DESTROYING A DEMOCRACY TO SAVE IT: DEMOCRATS CALL FOR THE DISQUALIFICATION OF DOZENS OF REPUBLICAN MEMBERS: Idiotic dystopia

The renewed calls for disqualifications may be simply reckless rhetoric timed for the anniversary of the riot... However, it is reason - not rage - that we need right now.

….

The assault to capitol the day 6 didn’t kill the death. It just did the opposite: resuscitate voting as core essence of democracy. IF SO: disqualification should start with those who commit Electoral Fraud, starting with billionaires who financed both Dems & REP parties, and the bureaucrats paid to miscounting votes, especially the members of the Electoral College. They destroy democracy long time ago and the current ones must go to Jail. Top bureaucrats of DEM-REP parties deserve to be jailed. Only socialist parties can do this job if they manage to create A- UNITED FRONT & B- a team of Lawyers to put this case in State Courts and Fed Courts too. The rest will be done by Nation revolt in street

====

SEATTLE POLICE OFFICERS FALSIFIED REPORTS ABOUT PROUD BOYS MOVING TOWARD 'CHOP': WATCHDOG

"The string of communications prompted many people to go grab firearms and the event transitioned from being peaceful to something entirely different..."

====

THE VACCINE IS A DUD, BUT THAT WON'T STOP PUSH FOR DIGITAL IDS

"All this illiberalism is couched in terms of a new kind of "sustainable," "inclusive," "equitable" quasi-utopian society..."

====

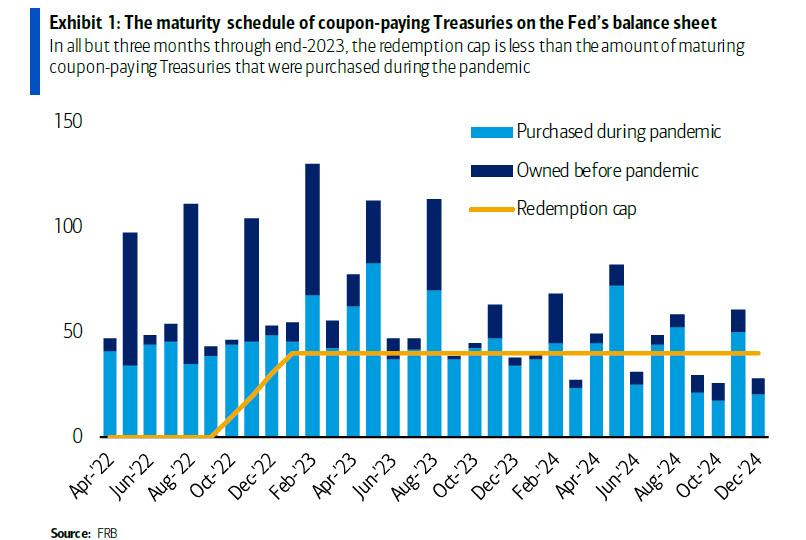

HERE'S WHAT THE FED'S QUANTITATIVE TIGHTENING WILL LOOK LIKE

by Tyler Durden

Here's What The Fed's Quantitative Tightening Will Look Like

To keep its balance sheet flat, the Fed would still have to purchase nearly $400BN worth of Treasuries in 2Q and 3Q 2022.

Fed's Bullard (who is a voting member this year) observed, the runoff could be passive, i.e., not involve actual selling but merely be the result of maturing securities held by the Fed.

In any case, in a note from BofA economist Aditya Bhave, he argues that the Fed’s balance sheet policy will remain accommodative for the next several quarters for several reasons:

- The Fed has more than doubled its balance sheet during the pandemic.

- Therefore it will have to reinvest a larger quantity of maturing Treasuries even while it is shrinking its balance sheet.

- BofA expects QT to start in 4Q 2022, but the stance of Fed balance sheet policy will remain more accommodative than it was before the pandemic through end-2023.

With regard to point two, a frustrated Steve Liesman pointed out yesterday that what the Fed is doing is a "historic absurdity" and noted that "the fed is talking about aggressively reducing its balance sheet while at the same time adding assets to that balance sheet. I think that's the monetary policy equivalent of a dog chasing its tail."

What markets want to know is what the Fed's QT will look like, and for the answer we again turn to BofA, whose strategists think the Fed will allow $10BN of maturing coupon-paying Treasuries to run off its balance sheet in the first month of QT (which they expect will start in October 2022). This “redemption cap” - shown in yellow on the chart below - should rise to $40bn by January 2023 and then remain at that level. They also assume a $30bn redemption cap for Agency MBS.

In total, this would allow the Fed’s balance sheet to shrink by $1.2tn through end-2024. They think the balance sheet could be cut further in future years, all the way down to $4.7tn, i.e. about 15% larger than its pre-pandemic level (spoiler alert: there is no way the market will allow this type of balance sheet shrinkage without a historic tantrum first).

A third view is that gross asset purchases are what matter. This is the view that BofA sympathizes with. In the "gross" world, the Fed replaces maturing assets via “add-ons” in Treasury auctions, or as Liesman put it, the Fed is adding to its balance sheet at the same time as it is shrinking it all the while it's chasing its tail. For example, if the Fed plans to re-invest $10bn in an auction, the Treasury would reduce the size of its auction by this amount and then allocate $10bn worth of securities to the Fed at the market-clearing price. Markets price in this mechanism: the larger the add-on, the less is the supply that markets have to absorb, and the higher would be the market-clearing price.

Theory aside, let's look at some numbers: since the Fed’s balance sheet has more than doubled during the pandemic, keeping it steady would require significantly more reinvestment than would have been the case before the pandemic. Specifically, to keep its balance sheet steady as a result if upcoming maturities, the Fed would have to purchase (i.e., reinvest) nearly $400bn worth of coupon-paying Treasuries in 2Q and 3Q 2022, of which 59% were bought during the pandemic. This, according to BofA and it is correct here, would buffer the impact of rate hikes. Recall that most banks are now forecasting three to four hikes this year, as the Fed responds to sticky high inflation.

What about QT?

The chart below compares BofA's QT forecast to the maturity schedule of coupon-paying Treasuries on the Fed’s balance sheet. The light blue bars represent Treasuries that were purchased in pandemic-era QE and the dark blue bars show those that were on the balance sheet pre-Covid. Quantities below the QT redemption cap (the yellow line) would run off the balance sheet while those above the cap would be reinvested (i.e., re-purchased)

See Chart:

The maturity schedule of Coupon paying treasuries on FEDs balance Sheet

https://cms.zerohedge.com/s3/files/inline-images/QT%20schedule%20BofA.jpg?itok=y1h75qj4

{kind=link}

Notice that in all but three months through end-2023, the redemption cap is less than the amount of maturing coupon-paying Treasuries that were purchased during the pandemic. Therefore in 2022 and 2023, reinvestments will generally exceed the amount of maturing assets that the Fed owned before Covid.

In other words, the likely path of reinvestment under QT would have amounted to QE relative to the pre-pandemic Fed balance sheet.

The bottom line is despite impending QT, the stance of the Fed’s balance sheet policy for the next couple of years should be more accommodative that it was pre-pandemic (as it continues to buy tens of billions in Treasuries just to keep its balance sheet from shrinking too fast), and as a final note, the above analysis excludes the additional liquidity support of roughly $1.5 trillion currently parked in the Reverse Repo facility which will slowly be drained in the coming quarters to make the impact of QT easier.

….

SOURCE: https://www.zerohedge.com/markets/heres-what-feds-quantitative-tightening-will-look

----

----

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China, RU, Iran search for State socialis, D rest in limbo

CHINA'S XI ORDERS MILITARY TO CREATE "ELITE FORCE" TO WIN WARS

Chinese leader Xi Jinping delivered this year’s mobilization orders to the regime’s military on Jan. 5, saying it must evolve into an elite force capable of winning any war.

====

SPUTNIK NEWS : https://sputniknews.com/

WW3? British Warship Collided With Russian 'Hunter-Killer' Submarine, Claims UK Defence Ministry

- Norwegian Vaccine Researcher Says Pandemic 'Over for Most', Health Authorities Beg to Differ

- Sweden Talks NATO With Finland as Supreme Commander Slams Russian Security Proposals

- Ted Cruz Tells Tucker Carlson It Was 'Frankly Dumb' to Call 6 January a 'Violent Terrorist Attack'

- Two Journalists Killed in Haiti After Interviewing Criminal Lord

- US, Japan to Collaborate on Developing Hypersonic Missile Defenses Genocide Bus

- Kazakh Presid to the Nation as Constitutional Order 'Mostly Restored in All Regions'

- January 6 Riot Exposed America’s Vulnerabilities to Disinformation

- DHS Warns US Law Enforcement of Extremist Calls Online on Jan. 6 Riot Anniv

- Dozens Gather Outside DC Jail in Support of Imprisoned US Capitol Rioters

- Sen. Leader Schumer Recounts Jan. 6 Chants: ‘There‘s the Big Jew, Let‘s Get Him‘

====

====

JAN 6 2022 PART 1-2 ND SIT EC y POL SPANISH ++

REBELION

Opin- EL DERECHO DE LA DERECHA A RE-EXISTIR Juan Montaño

Ecol S: MÁS ALLÁ DE GLASGOW Iain Bruce

Econ: balance 20 AÑOS DE ENTRADA DEL EURO Yago Álvarez

Ecuad: Desmontando el discurso minero de seguridad jurídica A A

2021: ALC entre dos modelos de economía y sociedad JJ P y M C

Nancy Fraser «El ‘capitalismo caníbal’ está en nuestro horizonte»

Julian Assange: MEX Y EL DERECHO DE ASILO Gerardo Villagrán

Caso Assange: El más grave ataque a la libertad de la prensa mund

Perú: La supuesta corrupción del Min de Educ en el Perú

En política la corrup es delito que envuelve a 2 (acusado y acusador)

Y aquí a 3-4, pues se apunta contra el Presid de Izq por prensa pagada

Panam: heridas abiertas por invasión y masacre USA de 1989 A V R

ARG: 2021, POBREZA, DEUDA y PROTESTA Daniel Campione

ARG Marchemos este 1 de feb para exigir renuncia de miemb d Corte

USA: Huelgas y moviliz por condic laborals resurgen tras décad de letargo

Chile: AMANECER CON ESPERANZA J J. Paz-y-Miño Cepeda

COL: EL TERCER CICLO DE LA VIOLENCIA Horacio Duque

Cuba: DESIGUALDADES VIVIDAS POR MUJERES RURALES

España REFORMA LABORAL NEOLIBERAL Miguel Medina

MX: crisis política del obradorismo y del régimen oligárquico M T

USA: Latente amenaza de guerra terminal Álvaro Verzi Rangel

USA: INFLACIÓN Jorge Majfud

África PIERDE LA CARRERA CONTRA EL HAMBRE

PAL: El “piano” de la muerte en la cárcel de Palmira Jean-Pierre

Mund: La perestroika jaló la historia Ariel Dacal Díaz

----

----

RT EN ESPAÑOL

- El presid de Kazajistán ordena abrir fuego contra los "terroristas" sin previo aviso https://actualidad.rt.com/actualidad/416146-presidente-kazajistan-ordena-abatir-terroristas

….

Violentas protestas en Kazajistán acaparan la atención mundial: ¿Qué pasa allí ahora? https://actualidad.rt.com/actualidad/416087-kazajistan-protestas-disturbios

….

Así responde Am-Lat ante aumento de casos de CV y presencia de variante ómicron https://actualidad.rt.com/actualidad/416044-latinoamerica-medidas-casos-variante-omicron-coronavirus

….

Google habría pagado millones de dólares a Apple para ser el buscador predeterminado https://actualidad.rt.com/actualidad/416019-google-pagar-apple-buscador-predeterminado-dispositivos

----

----

CROSS TALK https://www.rt.com/shows/crosstalk/

….

GLOBAL RESEARCH

Geopolitics & Econ-Pol crisis that leads to more business-wars from US-NATO allies

The Corona Crisis: Is the Tide Turning? “A Rapid General Awakening”? By Peter Koenig,

Gaslighting from the WHO By Steve Kirsch,

COVID, Mandatory Vaccinations and the University System BY Var Aut

The Politics of Abortion: Medical Science Advances Threaten Roe v. Wade By Renee Parsons

----

----

VOLTAIRE NET ORG

https://www.voltairenet.org/en

RUSSIA WANTS TO FORCE THE US TO RESPECT THE UN CHARTER

by Thierry Meyssan

SOURCE: https://www.voltairenet.org/article215199.html

----

----

DEMOCRACY NOW

Amy Goodman’ team

-Elie Mystal: AG Garland Must Be More Aggressive, Hold Trump & Allies Accountable for Insurrection

- “White Rage” Author Carol Anderson: GOP Attack on “Election Fraud” Really an Attack on Black Voters

- “Why Was the Federal Gov’t So Unprepared?” Newsweek Reporter William Arkin on Jan. 6

- Reform the Insurrection Act: Former Pentagon Adviser Says Trump Almost Used It to Subvert Election

====

====

No hay comentarios:

Publicar un comentario