ND JUN 6 19 SIT

EC y POL

ND denounce Global-neoliberal

debacle y propone State-Social + Capit-compet in Eco

ZERO HEDGE ECONOMICS

Neoliberal globalization is

over. Financiers know it, they documented with graphics

DEFENSE:

we got into WW3 Economy: Trump’ monarchy has absolute power

US

markets were mixed early on with the overnight weakness (Mexico and China)

ignored and bid into the green before the cash open. Small Caps and Trannies

(most exposed to short-squeeze) were red from the start but the rest of the

majors trod water holding modest gains (despite more Mexican tariff headlines)...

See Chart:

{kind=link}

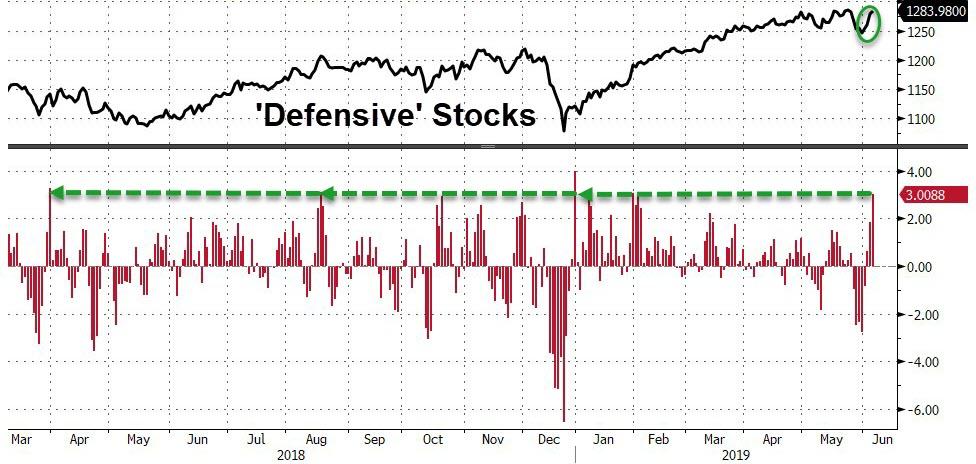

Defensive stocks are up 4 days in a row - notably

outperforming cyclicals in this ramp...

See Chart:

{kind=link}

This is

the biggest 4-day surge in

defensives since Dec 31st...

See Chart:

{kind=link}

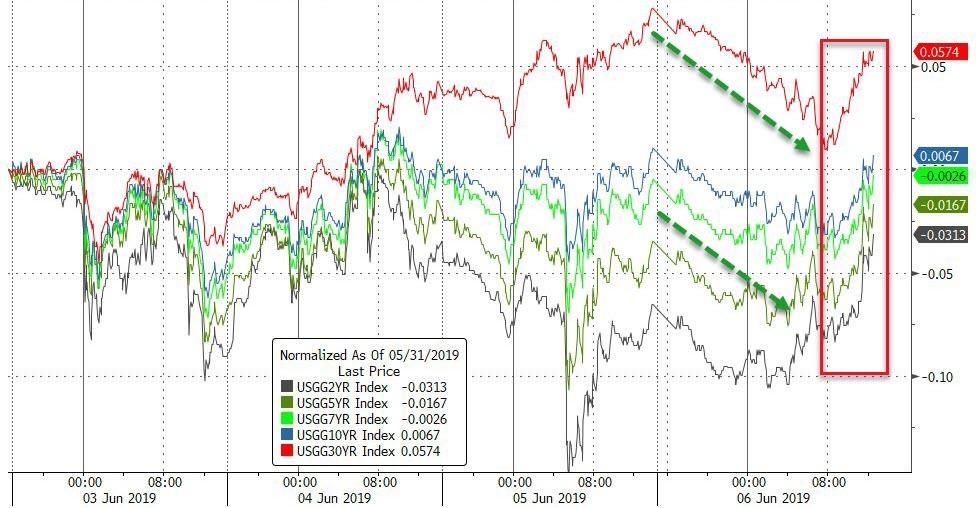

Bonds

were very mixed today with the action being the exact opposite of yesterday -

long-end outperforming notably...

See Chart:

{kind=link}

The

dollar index fell on the day, erasing yesterday's gains...

See Chart:

{kind=link}

The

peso spiked on headlines about delaying the tariffs (but slid back on reports

expecting tariffs to hit)

See Chart:

{kind=link}

NOTE -

stocks did not retrace like peso. Is this a sign of manipulation?

See chart:

{kind=link}

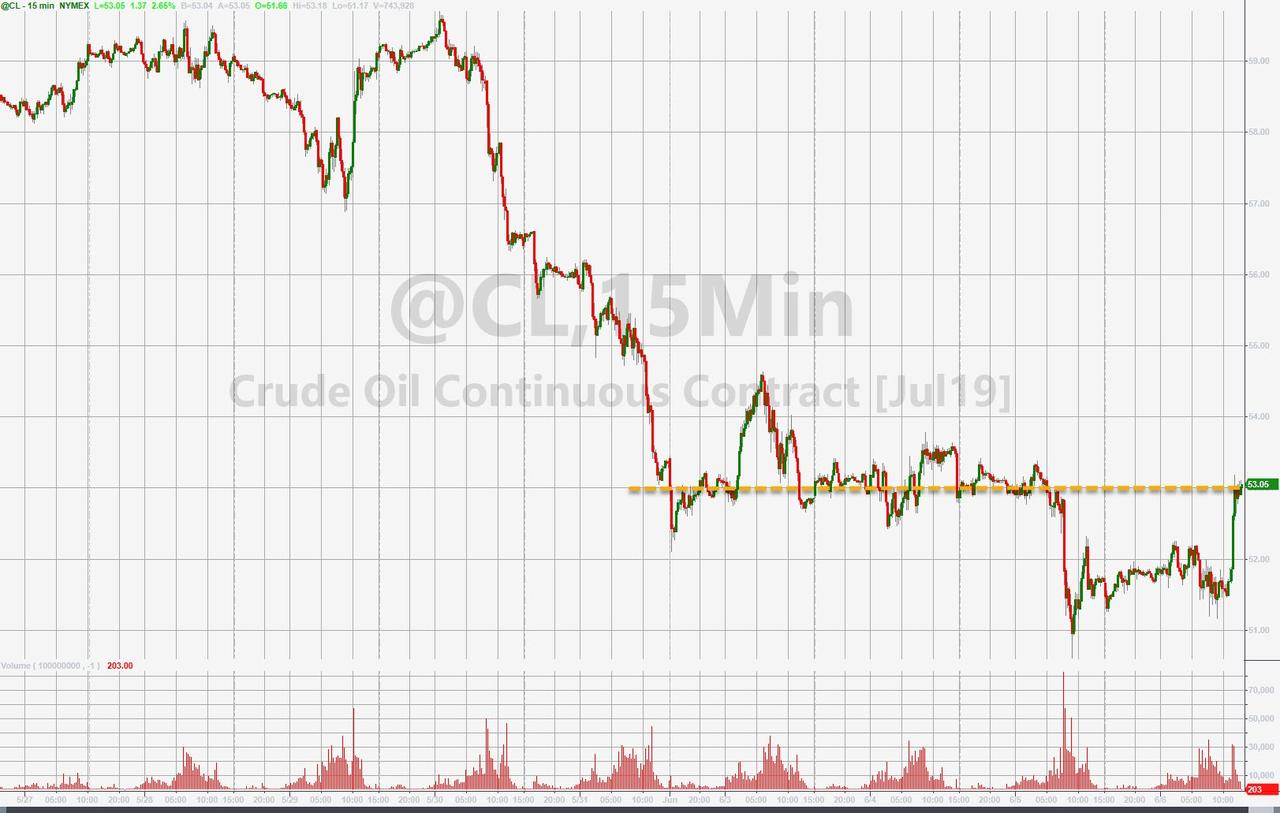

Oil

bounced on the day (after the tariff delay headlines) but some context is

worthwhile...

See Chart:

{kind=link}

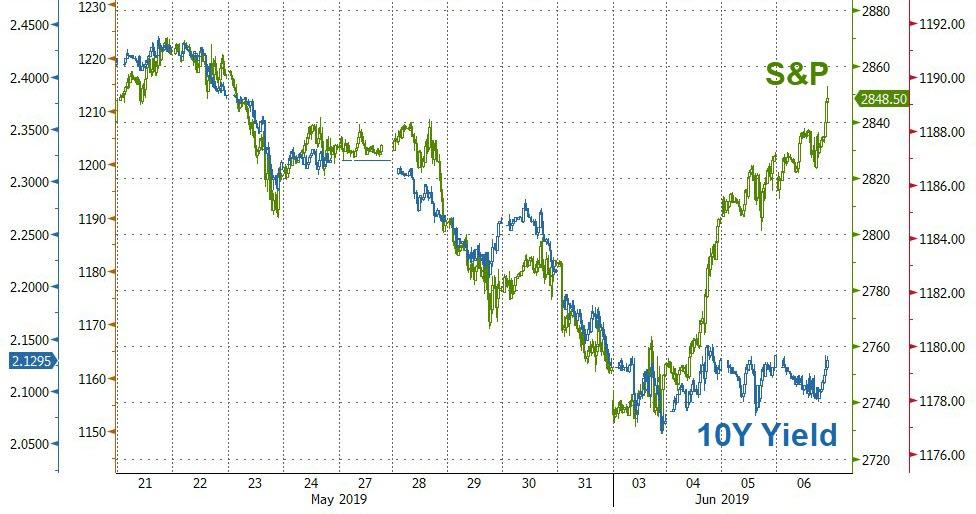

Finally,

after a string of dismal macro data, Bonds & Stocks remain drastically

decoupled...

See Chart:

{kind=link}

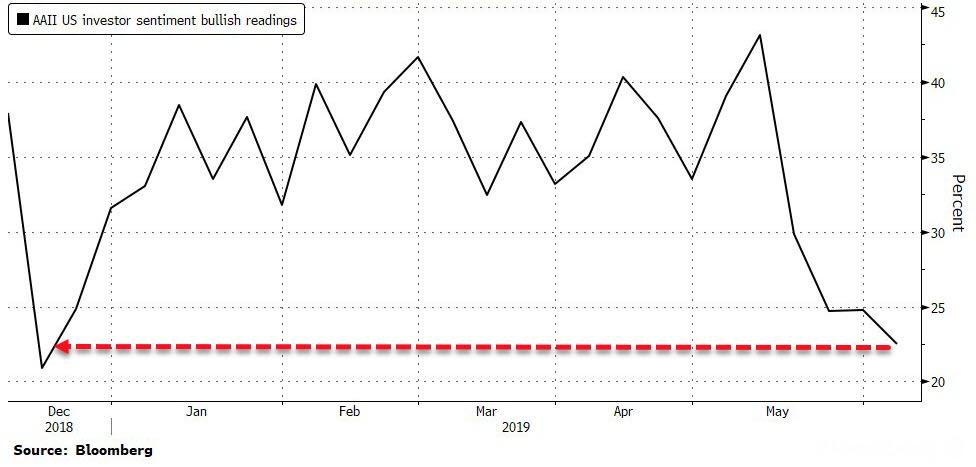

And, as

Bloomberg reports, Retail traders

are now the least bullish on the country’s equities since December, when

the S&P 500 sank to a 20-month low, according to a weekly

survey by the American Association of Individual Investors.

See Chart:

{kind=link}

WHAT

WILL PAYROLLS SAY?

….

----

----

"The

consumer in the bottom quintile has experienced 10% more cumulative

headline inflation and 15% more core inflation, than the consumer in the

top quintile income group"

By Tyler Durden Thu, 06/06/2019

First, the background details:

Official inflation has persisted below the 2% target this cycle,

coinciding with a drift lower in inflation expectations. Throughout this year,

Fed officials have mused about "makeup strategies," allowing

inflation to overshoot the target to compensate for past undershooting. At the

Fed's June policy framework conference in Chicago, Fed

Chair Powell noted that the models suggest this strategy would be

effective, but in reality there are major credibility questions as it requires

buy-in from households and businesses. In order to become credible,

a make-up strategy would need to be communicated in advance of a downturn, and

be followed by years of consistent policy. To

BofA,Powell's comments spray cold water all over a strict inflation averaging

regime.

However, an even more important dynamic that the Fed should consider

when pushing inflation above target-inflation: gains are felt unevenly by

income cohort. Empirical observations find that when

inflation picks up, the lowest income cohort generally experiences higher

inflation than the highest income group, because they spend more income share

on rent, food at home, and other inflationary items. This can be shown by

comparing the inflation rate of the bottom 20% and the top 20% income

distribution, reweighted by their spending shares.

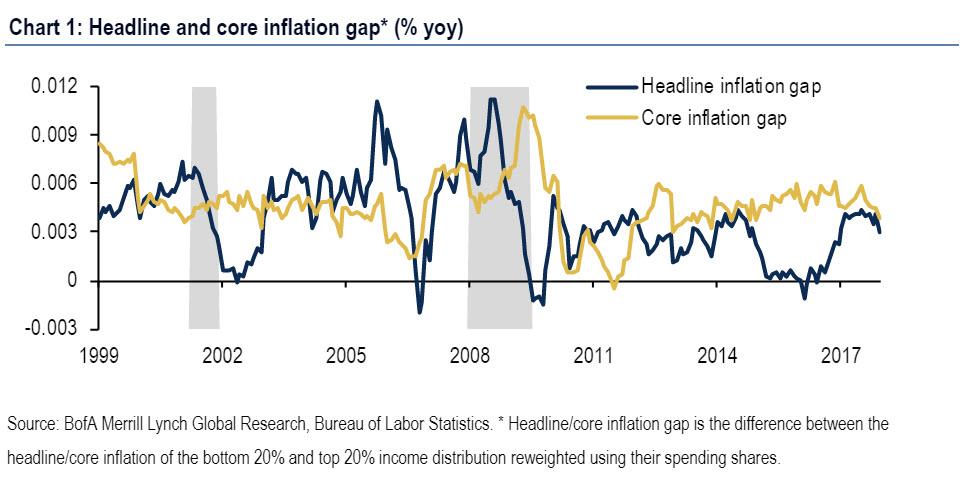

As shown below, inflation runs above for

lower income households given their spending composition.

See Chart:

Headline and “core inflation gap” (% YoY)

{kind=link}

There is a persistently positive headline and

core-excludes food and energy-inflation gap between the bottom 20% of the

income distribution and the top 20%. Since 1999, the consumer in the

bottom quintile has experienced 10% more cumulative headline inflation (0.39%

on average) than the consumer in the top quintile income group. They have

also experienced 15% more core inflation (0.47% on average), and the core

inflation gap has been more stable compared with the headline inflation gap.

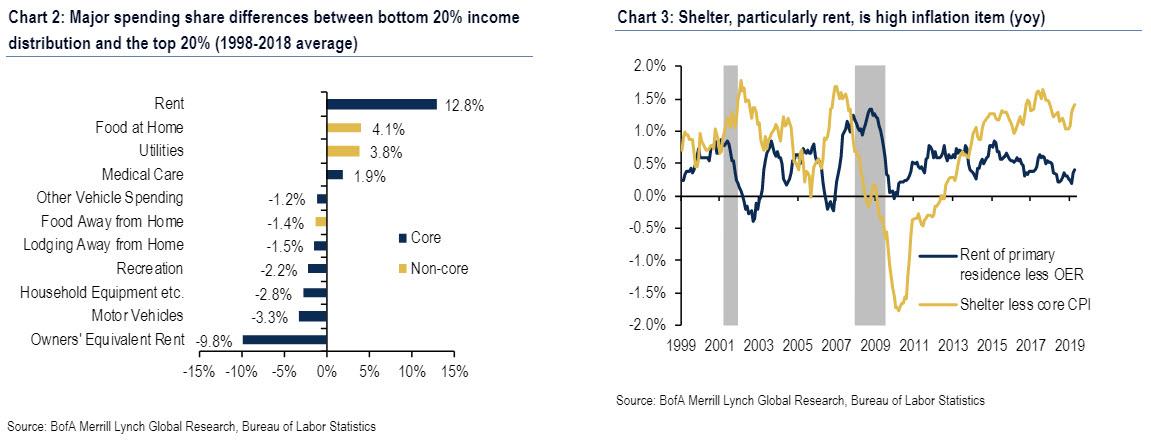

To understand these gaps, BofA compares the shopping carts of these two

groups (Chart 2). The largest difference within core lies in shelter. The lowest income consumer is much more likely to be a renter

than a homeowner, while the opposite is true for the highest income

consumer. Thus, rent of primary residence has a much larger share

in the former's spending basket, while owners' equivalent rent (OER) is bigger

in the latter. Rent of primary residence inflation

is persistently higher than OER inflation (Chart 3), thus a higher

weight in the former at the expense of latter would bias up aggregate

inflation. Also, taking into account the share differences of rent of primary

residence (+12.8%), OER (-9.8%), and lodging away from home (-1.5%) indicates

that shelter share broadly is a larger share of spending at the low-end (net

share difference around 1.5%, Chart 2 again). This

provides additional upside bias given that shelter inflation generally

runs hotter than broader core inflation, and is therefore a "high

inflation" category (Chart 3).

See Charts 2 & 3

{kind=link}

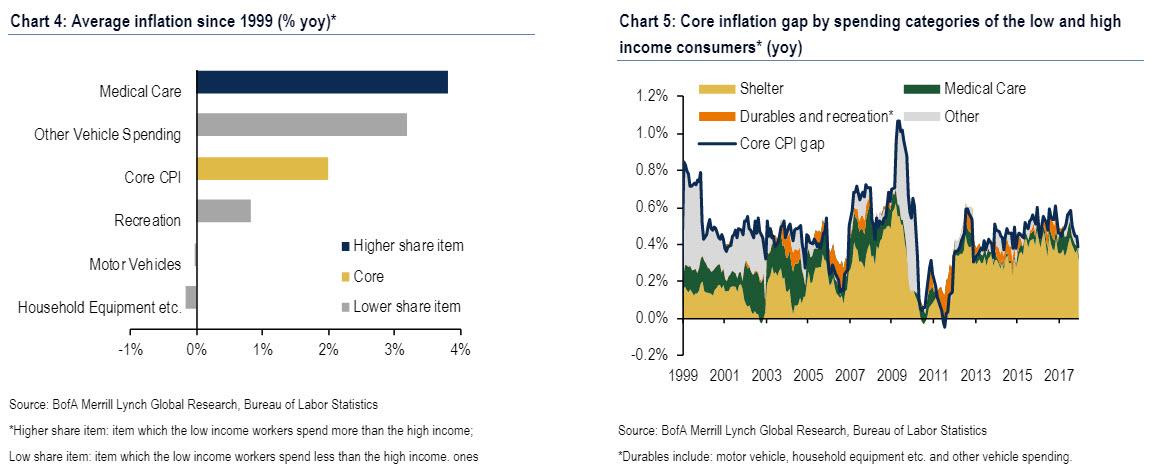

While shelter, or rather rent, is the most important spending category, there are also other categories that contribute to the core

inflation gap between the top and bottom income brackets, if on a smaller

magnitude. The lowest income consumers tend to spend more on medical

care services and less on things like motor vehicles, household equipment,

recreation, and other vehicle spending. Like shelter, medical care inflation

typically runs hotter than broader core inflation, averaging 3.8% since 1999

versus 2% for core CPI .:

With the exception of other vehicle spending, the other major core

categories where the lowest income consumer spent less than the highest income

consumer generally experienced more subdued inflation relative to core. Thus, the bottom bracket loses out relative to the top

bracket by allocating more of their spending to a high inflation category and

less of their spending to lower inflation categories.

See Charts 4 & 5

{kind=link}

Breaking down the core inflation gap, shelter

and medical care explained 91% of the inflation gap on average from 1999-2017

(Chart 5). That said, since

the financial crisis the contribution from healthcare has declined while

shelter has picked up and now explains most of the inflation gap. The rent is, indeed, too damn high... and it is hurting

the poor first and foremost.

BofA asked rhetorically, it "the fact that

higher inflation hurts the lowest income workers disproportionally might lead

people to question if monetary policy contributes to greater inequality." Well,

of course - in fact, former Fed Chair Bernanke pointed

out in 2015 that that was one of the major critiques of

quantitative easing. Two effects are often mentioned.

- The "income composition channel": People in lower income buckets primarily rely on wages for income, while people in higher income buckets will also be compensated with corporate equities. If expansionary monetary policies boost corporate profits more than they do wages, those with claims to ownership of firms will tend to benefit disproportionately, worsening income inequality.

- The "portfolio channel": Low-income workers tend to hold relatively more currency than high-income workers. Therefore, higher inflation would hurt the purchasing power of low-income consumers more than high-income, increasing consumption inequality

In short, not only is the Fed screwing the poor... it

is doubly screwing the poor!

In other words, in the grand scheme of

things the Fed's job is to focus on those pathways that make the rich richer,

even if in the process the poor become even poorer, and the US middle class

erodes.

Bottom line, the Fed's

apologists will say, "by stabilizing the business

cycle and thereby promoting job and wage growth, the Fed produces a positive

outcome for the lowest income cohort."

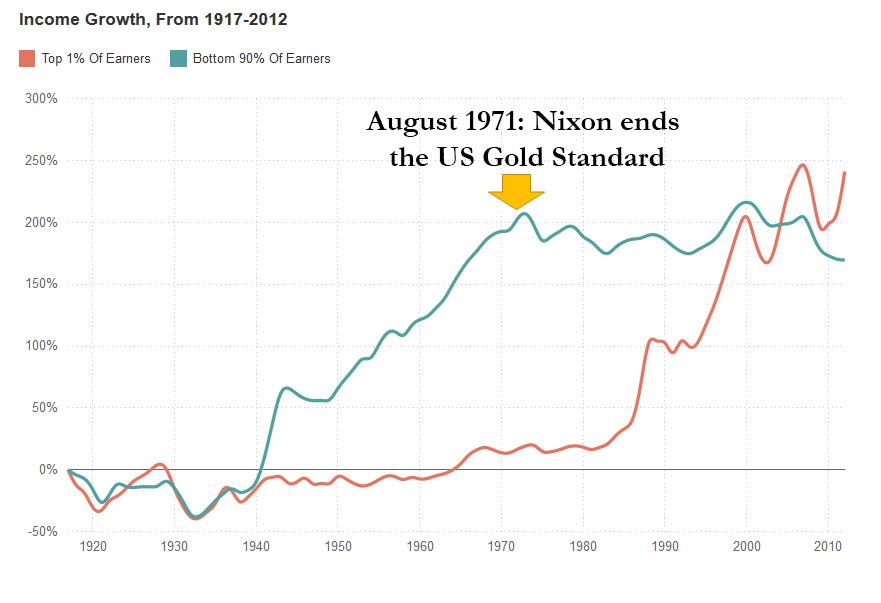

Incidentally, for those curious just what event catalyzed the

unprecedented divergence between America's haves and have nots, we provided

the answer over 4 years ago: the dramatic

ascent of the "Top 1%" of earners at the expense of the "Bottom

90%" started in the early 1970s... when Nixon ended the gold standard.

It is this monetary framework, more than anything, that

the current iteration of the Fed will do everything in its power to protect.

See Chart:

Income Growth from 1917-2012

{kind=link}

Should it be successful, one thing is certain:

the implementation of more "bubble" policies that create even greater

social inequality, one which - as the French discovered in the late 18th

century - inevitably culminates in revolution.

Which is, no matter how one gets there, THE END OF THE FED ..

it couldn't come fast enough.

….

SOURCE: https://www.zerohedge.com/news/2019-06-06/how-feds-new-monetary-policy-will-crush-americas-poorest

----

----

"If we

get a jump in claims and a bad report on Friday with jobs, I think the stock

market will be back below 2,700 and the bond yield could be below 2%."

In short, one can see why Wall Street is confused... and recent economic

data is not helping. As BMO's Ben Jeffery writes, there are anecdotes for both

the positive and negative side of the June employment report "with seven positive proxies and five negative

ones."

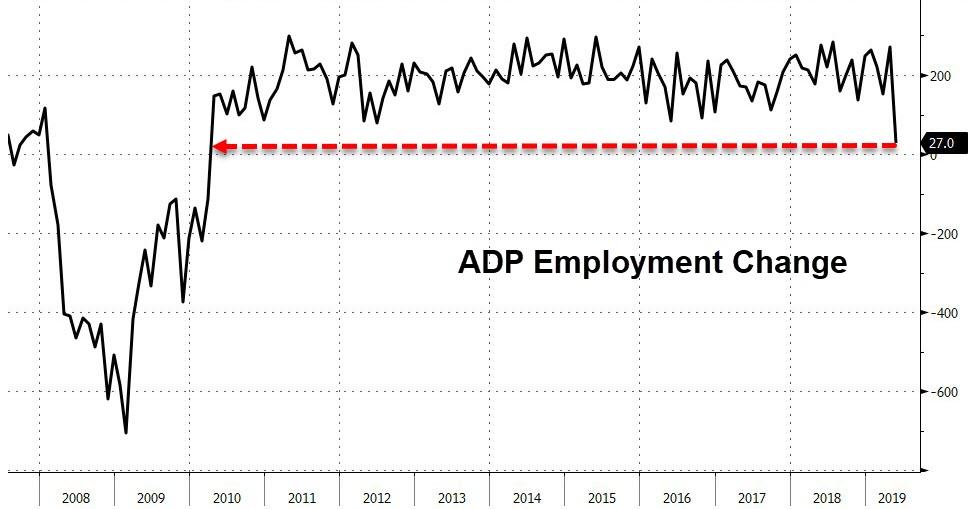

On one hand, in the plus column we have both ISM's employment components

rising from last month, and the labor differential has

climbed to the highest level since 2000. On the other hand, ADP showed the lowest read and largest miss since 2010 and the rise in

Challenger job cuts hints of some downside potential.

See Chart:

ADP Employment Change

{kind=link}

US jobs report is projected to show solid Labor

gains in payroll wages

See Chart:

{kind=link}

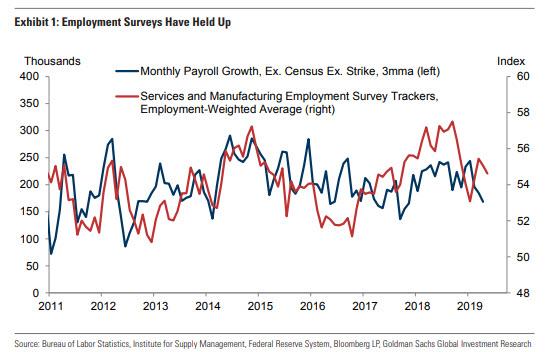

Some more observations on expectations: wages & ADP payrolls & ISM surveys

SeeChart:

{kind=link}

Ilya Feygin, senior strategist at WallachBeth

Capital LLC:

“If we get a strong jobs report, probably equities will decline

slightly because the probability of a rate cut would decline. And a good part

of this recent rally was due to more rate cuts priced. It also depends what

average hourly earnings are.”

….

----

----

Will the Federal Reserve be able to once again reignite “Ponzi”

borrowing to suspend that outcome?

Compare and Contrast

The tables below summarize two extreme economic models to exhibit how an

economy dependent upon “Ponzi” financing compares to one in which savings are

prioritized. In both cases, we show how the respective financial decisions

influence consumption, profits, and wages.

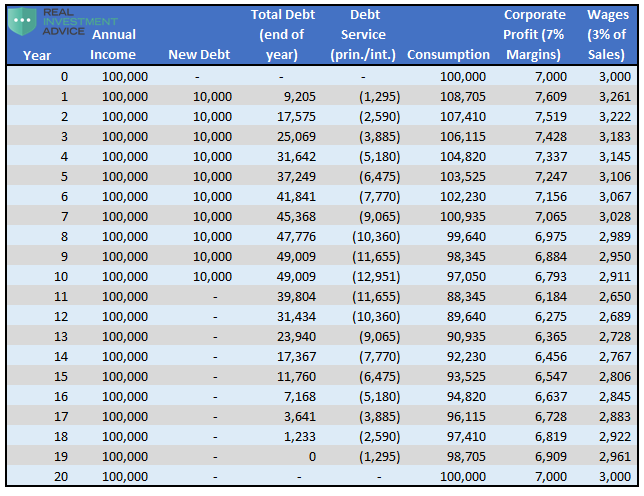

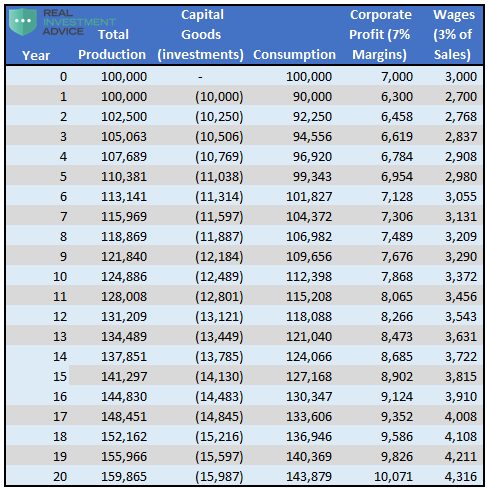

Table 1, below, is based on the assumption that

consumers spend 100% of their wages and borrow an additional amount equivalent

to 10% of their income annually for ten years straight. The debt amortizes

annually and is therefore retired in full in 20 years.

SEE table 1t:

{kind=link}

Assumptions: Debt is borrowed each year for the first ten

years at a 5% interest rate and ten year term, corporate profits and employee

wages are 7% and 3% of consumption respectively, annual income is constant at

$100,000 per year.

Table 2, below, assumes consumers spend 90% of

wages, save and invest 10% a year, and do not borrow any money. The table is

based on the work of Henry Hazlitt from his book Economics in One

Lesson.

See Table 2

{kind=link}

Assumptions: Productivity growth is 2.5% per year, corporate

profits and employee wages are 7% and 3% of consumption respectively.

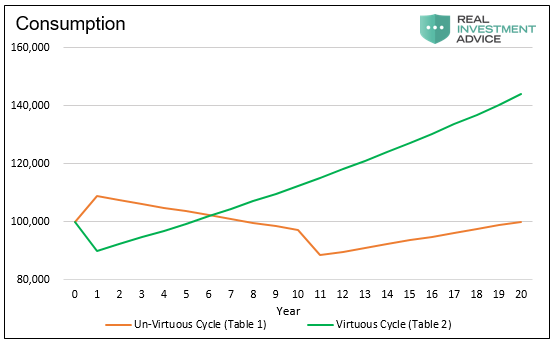

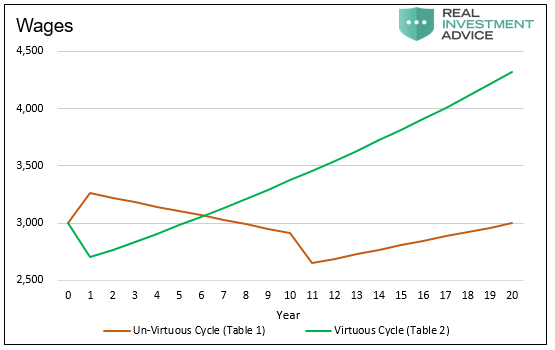

Table 1 is the U-VC and Table 2 is the VC. The tables illustrate that

there are immediate economic benefits of borrowing and economic costs of

saving. For example, in year one, consumption in Table 1 rises as a result of

the new debt ($100,000 to $108,705) and wages and corporate profits follow

proportionately. Conversely, table 2 exhibits an initial $10,000 decline in

consumption to $90,000, and a similar decline in wages and corporate profits as

a result of deferring consumption on 10% of the income that was designated for

saving and investing.

After year one, however, the trends begin to reverse. In the U-VC example

(Table 1), when new debt is added, debt servicing costs rise, and the marginal

benefits of additional debt decline. By year eight, debt service costs

($10,360) are larger than the additional new debt ($10,000). At that point,

without lower interest rates or larger borrowings, consumption will fall below

the income level.

Conversely, in the VC example (Table 2), savings and investments engender

productivity growth, which drives wages, profits, and consumption higher.

The graphs below highlight the consumption and wage

trends from both tables.

See Graphs: 1 Consumption:

{kind=link}

See Graph 2: Wages:

{kind=link}

As illustrated in both graphs, the short term justification for promoting

the U-VC is prompt economic growth. Equally important, the reason that savings

and investments in the VC are admonished is that they require discipline and a

period of lesser growth, profits, and wages.

Debt-fueled consumption is an expedient measure to

take when economic growth stalls and immediate economic recovery is demanded.

While the marginal benefits of such action fade quickly, a longer-term policy

that consistently encourages greater levels of debt and lower debt servicing

costs can extend the beneficial economic effects for years, fooling many

consumers, economists and business leaders into believing these activities are

sustainable.

Summary

The U.S. and many other countries are forced to deal with the consequences

of economic policy actions, borrowing, and consumption behaviors from years

past. While the present economic situation is troubling, leadership is

obligated to reflect on past choices and move forward with changes that are in

the best interest of the country and its entire population. As our title

suggests, we can continue to try to pull consumption forward and further harm

future growth, or we can save and reward future generations with productivity

gains resulting in greater economic growth and prosperity.

Shifting direction, and

“paying forward,” via more savings and investments and the deferral of some

consumption, comes with immediate negative consequences to wages, profits, and

economic growth. Nothing worth having is easy, as the saying goes.

….

----

----

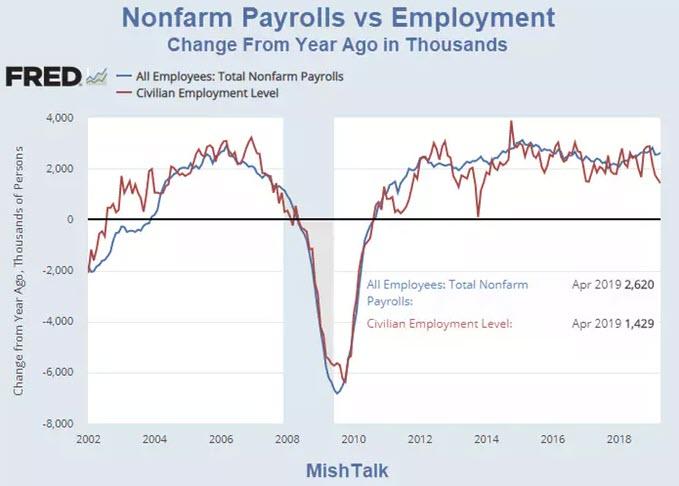

In the past year alone, the difference between jobs and

employment is a whopping 1,191,000. That's a discrepancy of 99,250

every month, in favor of jobs...

See Chart:

Nonfarm payrolls vs Employment

{kind=link}

….

----

----

US DOMESTIC

POLITICS

Seudo democ duopolico in US is obsolete; it’s full of frauds & corruption.

Urge cambio

... great wars and engineered economic collapse are their

primary tools to condition the masses to abandon their natural social

and biological inclinations towards individualism and tribalism

and embrace the collectivist philosophy.

The first assumption people make is that that current

system is the ideal globalist system – IT'S NOT EVEN CLOSE.

To summarize:

For at least the past century the globalists have been pursuing a true

one world system that is not covert, but overt. They want conscious public

acceptance of a completely centralized global economic system, a single global

currency, a one world government, and a one world religion (though that particular issue will require an

entirely separate article).

Continue reading at

….

SOURCE: https://www.zerohedge.com/news/2019-06-06/next-stage-engineered-global-economic-reset-has-arrived

----

----

"The control exercised over our awareness is

universal...not only is our

understanding of the economycontrolled by manipulation of our minds, but

also the markets themselves are controlled by official intervention..."

The America I grew up in was an opportunity society. There were ladders of upward

mobility that could be climbed on merit alone without requiring family status

or social and political connections. Instate college tuition was

low. Most families could manage it, and the students of those

families that could not afford the cost worked their way through university

with part time jobs. Student loans were unknown.

That America is gone.

The few economists capable of thought wonder about the high

price/earnings ratios of US stocks and the 26,000 Dow Jones when stock

buy-backs indicate that US corporations see no investment

opportunities. How

can stock prices be so high when corporations see no growth in US consumer

income that would justify investment in the US?

….

We live in a Matrix of

Lies in which our awareness is controlled by the explanations we are given. The

control exercised over our awareness is universal. It applies to

every aspect of our existence. In the article above I showed that

not only is our understanding of the economy controlled by manipulation of our

minds, but also the markets themselves are controlled by official intervention.

In brief, you can believe nothing that you are officially told. If you desire truth, you

must support the websites that are committed to truth.

….

----

----

FASCISTIC CONTROL OF THE PRESS IS ON:

Maybe a better answer for @Jack and Twitter would be to spend less time

policing the web and more time wondering why AOC is so easy to parody to

begin with...

====

THE FOREIGN MARKET IS ALSO CONTROLLED:

"When

faced with more margin pressure, what do you have to do? You have to address

what fixed costs you can remove."

====

"The

level in the chocolate cakewas

higher: more than 250 times the

only federal guidelines..."

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

Global depression is on…China,

RU, Iran search for State socialis+K-, D rest in limbo

...wars, particularly world wars, are often

catalyzed by those with a globalized agenda as a way to influence

the masses to abandon concepts like individualism, nationalism, free markets

and sovereignty, and to embrace

collectivism and total globalization.

====

Nasdaq futures have tumbled back into

the red following remarks from President Trump that he isconsidering extending tariffs to China on the

remaining $300 billion of goods.

====

"Our talks with China, a lot of

interesting things are happening. We’ll see what happens... I could go up

another at least $300 billion and I’ll do that at the right time."

====

Disappointingly, for Trump, the deficit with China increased $2.1

billion to $29.4 billion in April, with US

exports to China plunging back near 9 year lows.

….

Esta claro que lo que hace Trump es disparase a los zapatos y pronto su

econpmia no va a poder caminar. Culpar a china .. seria lo mas ridiculo

====

Blackmail on MX for Monday..

this is unfair.. just close the embassy .. move all US t-out

"...position

has not changed, andwe are still moving

forward with tariffs at this time.”

====

El chantaje de las tarifas es una humillacion a

la soberania de MX . The only choice for MX is getting the support of

RU-China & close the US embassy & cut relation with US

"We are optimistic because we had a good

meeting with respectful positions from both parts..."

….

Estamos en visperas del WW3.. MX no necesita del US pero debe reclamar su

neutralidad frente a la ONU. La neutralidad implica la salida immed de US troops

====

SPUTNIK

and RT SHOWS

GEO-POL n GEO-ECO ..Focus on neoliberal expansion via wars

& danger of WW3

----

----

NOTICIAS

IN SPANISH

Lat Am search f alternatives to

neo-fascist regimes & terrorist imperial chaos

REBELION

Mund: ¿Paz? Stephan Kaufmann

====

ALAI ORG

====

RT EN ESPAÑOL

- México se compromete con EE.UU. a desplegar 6.000 efectivos de la Guardia Nacional en la frontera con Guatemala

- Aranceles y 'crisis migratoria': Así va el pulso entre EE.UU. y México

- ¿Por qué los "sospechosos" ingresos de un ministro de la Corte sacuden la política en México?

- EE.UU. habría decidido dejar de entrenar a pilotos turcos en los F-35 por la compra de los S-400 rusos por Ankara

- Estas son las ocho nuevas funciones más útiles del próximo iOS 13

- Trump: "Con el respaldo de los demócratas haríamos que México se doble como un paraguas"

- Trump a México: "Cuando eres la alcancía a la que todos roban durante 25 años, los aranceles son una cosa hermosa"

- Keiser Report " US se volvio loco al inic guer com con Méx, China y Europa"

----

----

INFORMATION

CLEARING HOUSE

Deep on the US political

crisis: neofascism & internal conflicts that favor WW3

-Trump & NATO warmongers proclaim peace By Finian Cunningham

-Smearing China By Kim Petersen

-N- American, European Public: Finally Wake

Up, Damn It! By Andre Vltchek

-The State of the Economy By Paul Craig Roberts

-Donald Trump in the role of his life By César Chelala

-UN Special Rapporteur on Torture warns Julian

Assange could die in prison

By Kevin Reed FREE JULIAN ASSANGE

By Kevin Reed FREE JULIAN ASSANGE

-----

----

COUNTER

PUNCH

Analysis on US Politics &

Geopolitics

Lawrence

Davidson Cover

Ups and Truth Tellers

George

Ochenski What

Will It Take to Stop Trump’s Climate Policy Insanity?

Dean

Baker The

Wonderful World of Free Market Drugs

Binoy

Kampmark Cults of

Impeachment

Michael

T. Klare The

Pentagon’s Spoiling for a Fight … But With China, Not Iran

Thomas

Knapp The

First Amendment Protects Ex-Politicians Too

----

----

GLOBAL

RESEARCH

Geopolitics & Econ-Pol

crisis that leads to more business-wars from US-NATO allies

----

----

DEMOCRACY

NOW

Amy Goodman’ team

----

----

PRESS

TV

Resume of Global News described by Iranian observers..

----

===

No hay comentarios:

Publicar un comentario