ND

JUN 25 19 SIT EC y POL

ND denounce Global-neoliberal debacle y propone State-Social

+ Capit-compet in Eco

ZERO HEDGE ECONOMICS

Neoliberal globalization is over. Financiers know it, they

documented with graphics

BONDS,

BITCOIN, & BULLION JUMP; STOCKS DUMP ON POWELL-PULLBACK, TRADE-TALK

By Tyler Durden

Ugly US housing and confidence data

did not help but the cash open saw immediate selling of the modest overnight

gains. The ugly data sent the US Macro Surprise Index near its lowest since

June 2017...

See Chart:

S&P vs US Macro SURPRISE iNDEX

{kind=link}

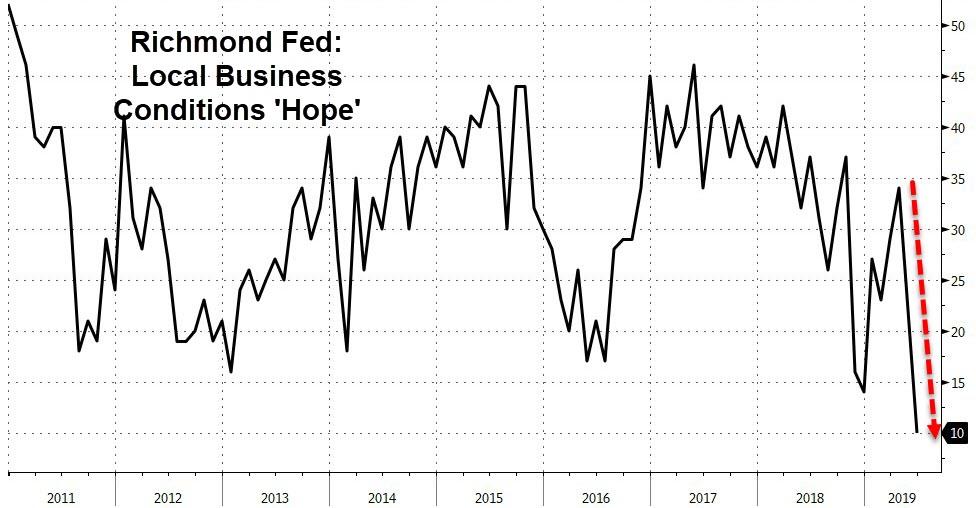

And while Richmond Fed's headline beat, expectations for

local business has crashed to a record low... (which seems very odd considering the Richmond Fed

head said today that "US Consumer dynamics remain great.")

See Chart:

{kind=link}

Then these hit and spoiled the party...

- 1230ET Bullard - no need for 50bps

- 1300ET Powell - monitoring, won't bow to political pressure

- 1330ET Trump-Xi meeting at G-20 not expected to produce a deal

All of which sent stocks lower for the second day... Trannies are the week's worst performer followed by

Nasdaq and Small Caps. For now The Dow is doing best but still lower since

quad-witch...

See Chart:

{kind=link}

Not a pretty day at all...

See Chart:

{kind=link}

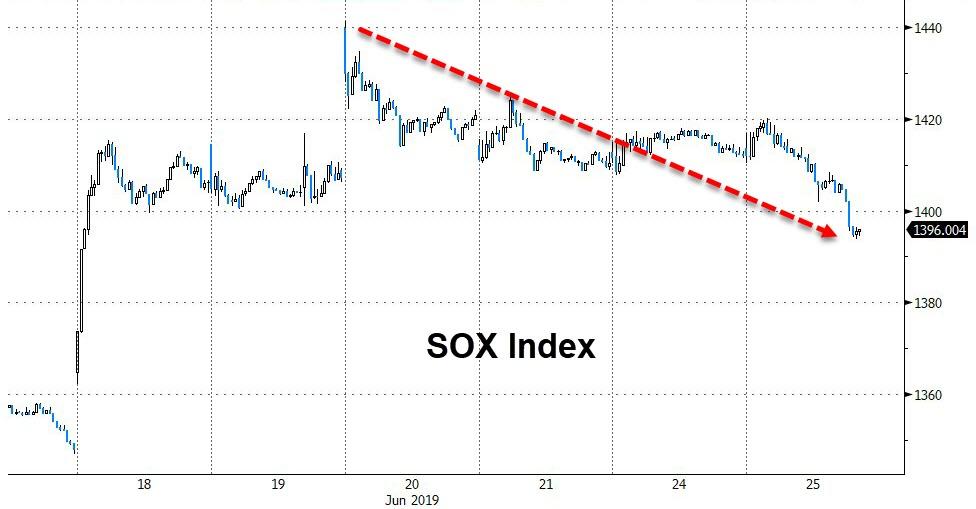

Winners of June have been losers

this week...

See Chart 1: S&P

Tech

{kind=link}

See Chart 2: SOK Index

{kind=link}

See Chart 3: Home builders

{kind=link}

VIX and Stocks remain decoupled...

See Chart: S&P vs VIX (inv)

{kind=link}

As July odds for a 50bps rate-cut

swung violently from 40% (pre-Bullard) to 16% (post-Powell) and back up to 26%

after the 'no trade-deal' news...

See Chart:

July Rate-Cut Odds

{kind=link}

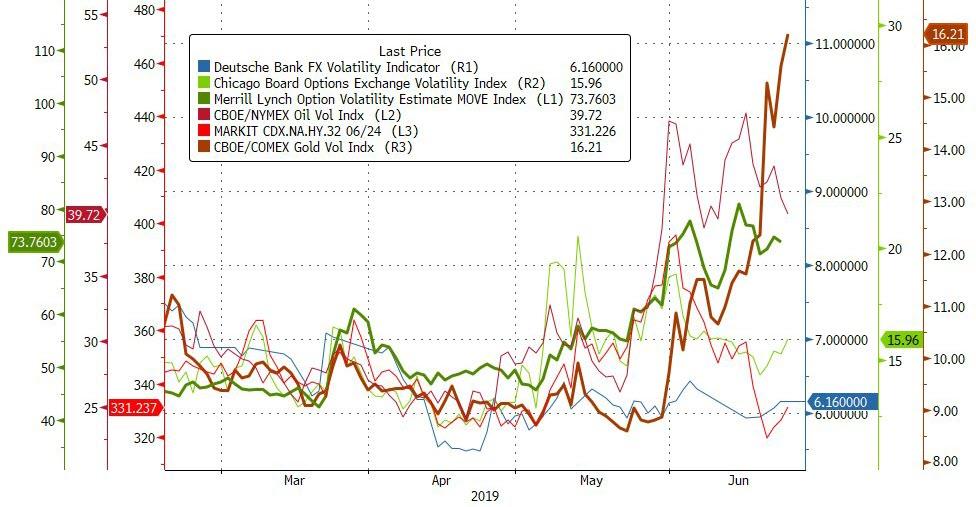

Credit markets have seen notable

decompression in the last few days...

See Chart:

{kind=link}

Treasury yields continued to fade

today except flat 2Y (despite a spike on Bullard headlines)...

See Chart:

{kind=link}

10Y yields tumbled below 1.98%...

See Chart:

{kind=link}

The dollar spiked today on

Bullard/Powell but faded on trade and in context to the post-FOMC move, it was

nothing...

See Chart:

FOMC vs. Bloomberg Dollar Index

{kind=link}

Gold was a little noisy intraday on

the FedSpeak (pushing the dollar around) but held gains breaking to new 6-year

highs overnight...

See Chart:

{kind=link}

Gold's "VIX" soared to 3

year highs, decoupling from other asset-classes...

{kind=link}

Finally, don't forget, there's only

one thing that matters...

{kind=link}

And if The Fed doesn't pay up and

give-in to the market's 50bps demands, the jaws of death will snap shut...

See Chart:

S&P vs. 10

Y UST Yield

{kind=link}

….

----

----

Since June 2009 Americans have lived in the

false reality of

a recovered economy. Various fake news and manipulated statistics have been

used to create this false impression...

However, indicators that really count have not supported the

false picture and were ignored.

For example, it is normal in a recovering or expanding

economy for the labor force participation rate to rise as people enter the work

force to take advantage of the job opportunities. During the

decade of the long recovery, from June 2009 through May 2019, the labor force

participation rate consistently fell from 65.7 to 62.8 percent.

See Chart:

{kind=link}

Another

characteristic of a long expansion is high and rising business investment.

However, American corporations have used their profits not for expansion, but

to reduce their market capitalization by buying back their stock. Moreover, many have gone further and

borrowed money in order to repurchase their shares, thus indebting their

companies as they reduced their capitalization! That boards,

executives, and shareholders chose to loot their own companies indicates that

the executives and owners do not perceive an economy that warrants new

investment.

How is the alleged 10-year boom reconcilled with an economy

in which corporations see no investment opportunities?

Over the course of the alleged

recovery, real retail sales growth has declined,

standing today at 1.3%.

This figure-not copied- is an overstatement, because the

measurement of inflation has been

revised in ways that understate inflation.

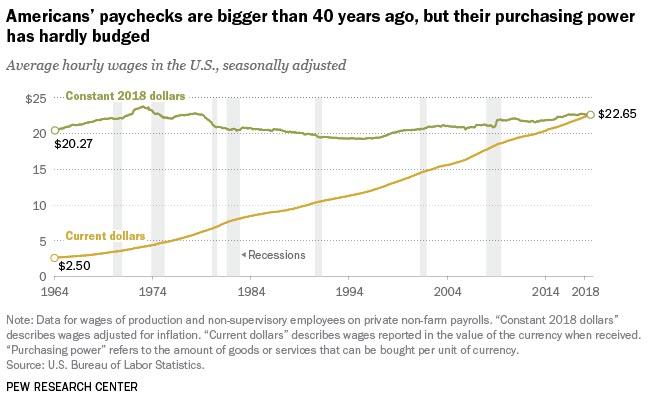

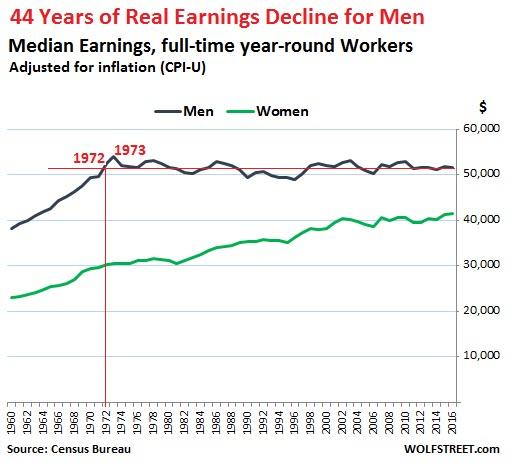

Real retail sales cannot grow

when “for most U.S.

workers, real wages have barely budged in decades.”

See Chart:

American paychecks are bigger than 40 years ago

{kind=link}

See Chart:

{kind=link}

The propagandistic

3.5% unemployment rate (U3) does not include any of the millions of discouraged

workers who cannot find jobs. The government does have a

seldom reported U6 measure of unemployment that includes short-term discouraged

workers. As of last month this rate stood at 7.1%, more than double

the 3.5% rate. John Williams of shadowstats.com continues

to estimate the long-term discouraged workers, as the government formerly

did. He finds the actual US rate of unemployment to be 21%.

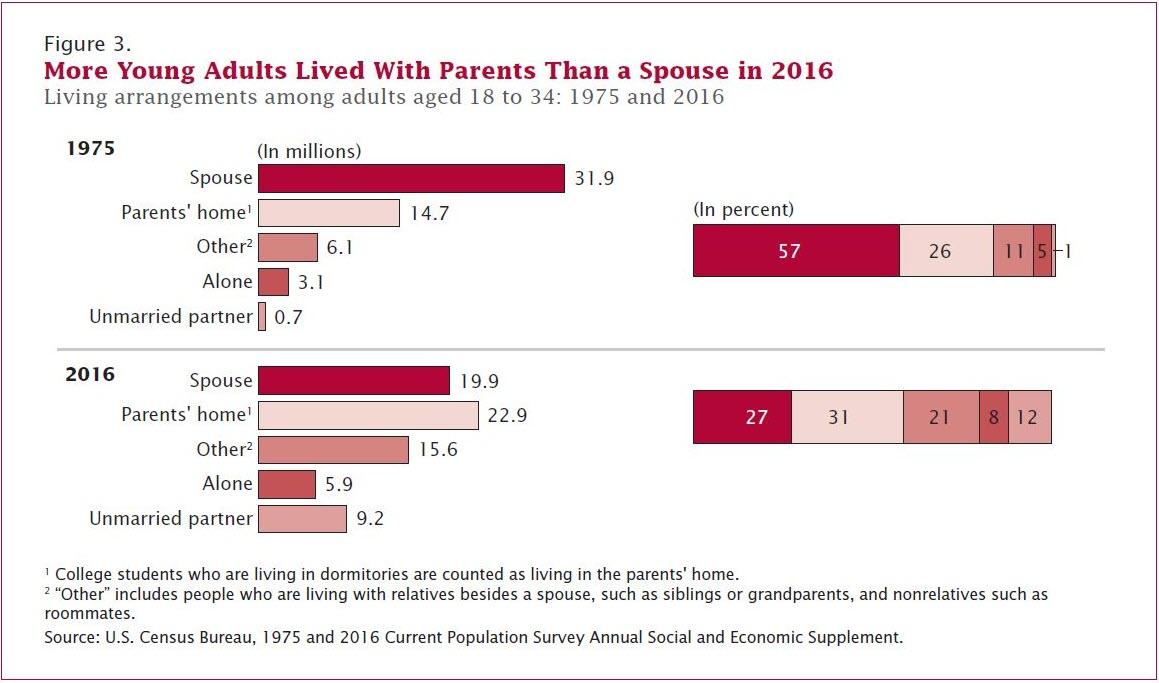

The 21% rate makes sense in light of

Census Bureau reports that one-third

of Americans age 18-34 live at home with parents because they can’t earn enough to support an independent

existence.

See Charts:

{kind=link}

See Chart:

{kind=link}

A

country with the massive indebtedness of the US government would quickly be

reduced to Third World status if the value of the dollar collapsed from lack of

demand.

SEE Chart:

{kind=link}

There are many countries in the world that have bad

leadership, but US leadership is the worst of all. Never very good,

US leadership went into precipitous and continuous decline with the advent of

the Clintons, continuing through Bush, Obama, and Trump. American credibility is at a low point.

Fools like John Bolton and Pompeo think they can restore credibility by blowing

up countries. Unless the dangerous fools are fired, we will all have

to experience how wrong they are.

Formerly the Federal Reserve conducted monetary policy with

the purpose of minimizing inflation and unemployment, but

today and for the past decade the Federal Reserve conducts monetary policy for

the purpose of protecting the balance sheets of the banks that are “too big to

fail” and other favored financial institutions. Therefore, it is

problematic to expect the same results.

- Today it is possible to have a recession and to maintain high prices of financial instruments due to Fed support of the instruments.

- Today it is possible for the Fed to prevent a stock market decline by purchasing S&P futures,...

- ...and to prevent a gold price rise by having its agents dump naked gold shorts in the gold futures market.

Such

things as these were not done when I was in the Treasury. This type of intervention originated in the

plunge protection team created by the Bush people in the last year of the

Reagan administration. Once the Fed learned how to use these instruments,

it has done so more aggressively.

Market

watchers who go by past trends overlook that today market manipulation by

central authorities plays a larger role than in the past. They

mistakenly expect trends established by market forces to hold in a manipulated

economic environment.

….

SOURCE: https://www.zerohedge.com/news/2019-06-25/paul-craig-roberts-exposes-diminishing-american-economy

----

----

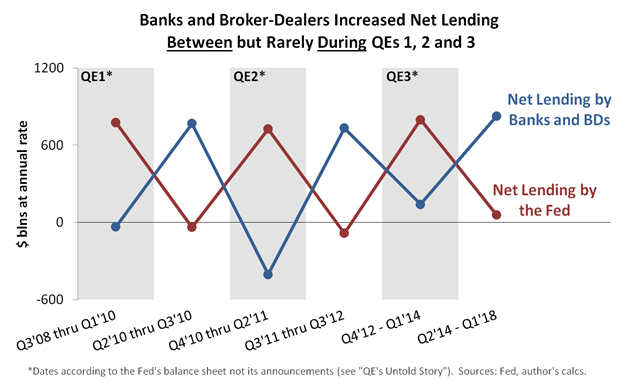

by Tyler Durden

It doesn’t take much calculation to see that the Fed’s position on

quantitative tightening (QT) is blatantly

inconsistent with its position on quantitative easing (QE)...

Here are the answers in chart form:

See Chart:

{kind=link}

Awkwardness

Alert: Here Comes a Chart that Really Excites Me

Two questions that seemed reasonable to ask:

- How rapidly do banks and broker–dealers (BDs) expand credit during QE periods (QE1, QE2 and QE3) compared to QE pauses (all other times)?

- How does bank and BD credit expansion compare to the Fed’s credit expansion during the same periods?

Here are the answers in chart form:

See Chart: WHY SAME CHART??

BLOCKED OR INTENTION DISTORTION?

https://www.zerohedge.com/s3/files/inline-images/testing-the-Feds-narrative-1_thumb-1.png?itok=Qjc6VyI7

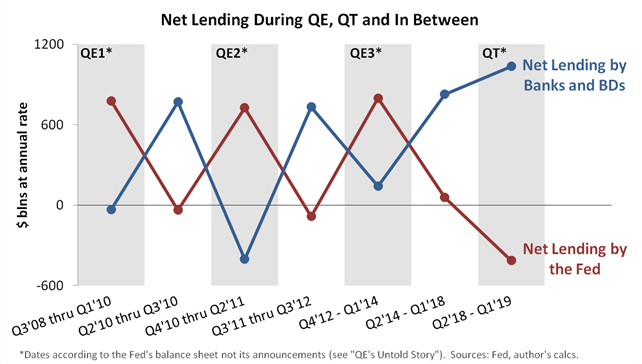

All of which brings us from QE to QT. As of this month, the

Z.1 shows four consecutive quarters of the Fed reducing its

net lending, thanks to QT. So the argyle effect is necessarily over, because

the Fed no longer alternates between only two options—QE and not-QE. The

pattern has to change, but to what? Well, here’s the answer:

See Chart:

{kind=link}

Three

Possibilities

So what

exactly does the new QE–QT pattern tell us? I’ll suggest three

possibilities, ordered from my least likely to my most likely:

- QT might have caused the total amount of credit supplied to the nonfinancial sector to fall, a result that would be intriguing largely because of what it would say about the central bank’s expectations. If the private financial sector fully offset QE’s credit creation but not QT’s credit contraction, which is the conclusion you might reach if relying on nothing but the chart, then Bernanke and Yellen got it completely backwards. You’ll never see that conclusion in the Wall Street Journal, for the reasons noted above, but it actually fits the data.

- We might not have enough QT data to reach a firm conclusion just yet. In other words, we might find that the picture changes with a few more QT quarters, especially as the volatility of these figures is quite high. That’s why I waited for four quarters of data before publishing my chart, but four still might not be enough.

- Total net lending might have declined over the last four quarters even without QT, such that any QT effects were negligible, notwithstanding my chart. Instead, debt-saturated borrowers might have decided to take a rest after nine years of expansion and independently of monetary policy. This view lines up nicely with the Fed’s loan officer survey, which shows weakening demand for most types of loans during the last four quarters. It’s also consistent with the idea that monetary policy makers neither manufacture nor extinguish creditworthy borrowers, who travel to loan and underwriting desks from all corners of the economy, just not from the front steps of the Eccles building as the Fed adjusts its bond holdings.

For what

it’s worth, my last point above ties into what I believe to be one of the

biggest flaws in the Fed’s make-up. That is, scholars like Bernanke and Yellen

reason from theories that require people to respond slavishly and robotically

to every adjustment in public policy, however odd, circular or obscure the

adjustment might be. In Bernanke

and Yellen’s world, it’s no exaggeration to say that central banks really do

manufacture creditworthy borrowers, as if the term open market account

describes a freakish assembly line, not a simple bond portfolio.

Bottom

Line

You’ll form your own

views on all of the above, but my advice is to filter the Fed’s narrative with

a healthy skepticism, however deferentially the media chooses to endorse it. I’m not saying the narrative is always wrong, just that

monetary policy is notoriously difficult to evaluate. But not

impossible—the Fed’s data can help separate fact from fallacy. Dig into the

Z.1, and you might find that the best reality-check is a single chart—call it

the Burberry truth—modest in ambition but scintillating nonetheless.

….

----

----

Retail investors will soon be able to trade CDS and CDOs (both cash and

synthetic). What can possibly go wrong?

See Chart:

NOW THE

CHART IS BLOCKED

OPEN THE TITLE ABOVE

TO SEE IT

----

----

Unfortunately, the world is now entering

a new “dis-saving” phase, as the baby boomers start to live off their past

contributions into 401(k), pension plans and the like. History suggests

this phase is likely to be inflationary...

It doesn’t make sense to copy charts

Open the title above

----

----

US

DOMESTIC POLITICS

Seudo democ duopolico in US is obsolete; it’s full of frauds

& corruption. Urge cambio

In a speech today, Fed Chair Jerome Powell took a swipe at Trump, then patted himself and the Fed on the back...

====

Beginning

in 2008 and continuing through 2014, precious metals traders employed by MLCI

schemed to deceive other market participants by injecting materially false and

misleading information into the precious metals futures market

====

"digital

demand for all things Trump dropped 29%..."

====

====

"The

legislators assert Trump’s receipt of benefits through his far-flung business

holdings -- including his luxury hotel just blocks from the White House --

violates a U.S. constitutional provision barring American presidents from

accepting so-called emoluments."

====

US-WORLD ISSUES (Geo Econ, Geo Pol & global Wars)

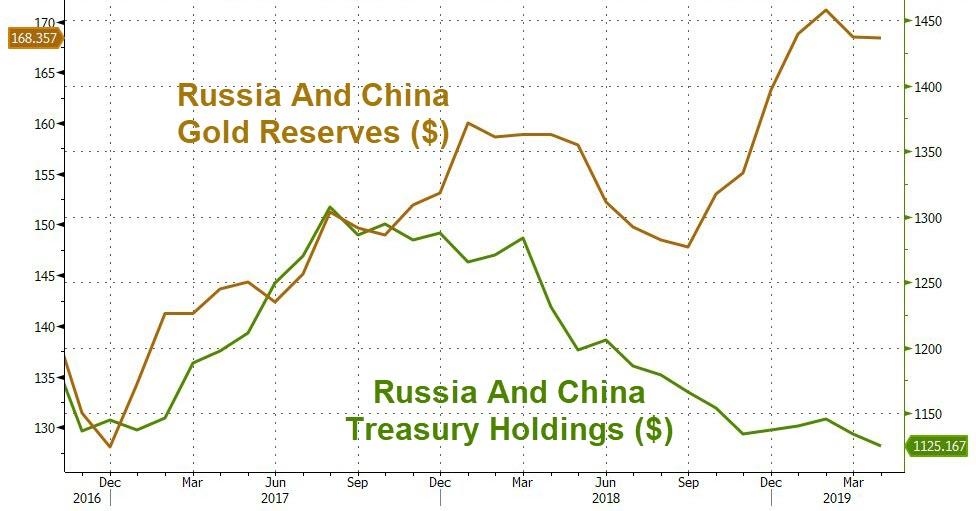

Global depression is on…China, RU, Iran search for State

socialis+K-, D rest in limbo

... countries with "geopolitical

tensions with the US" are buying everything...

====

"You were really worried about 150 people?"

====

La Carrera armamentista en el otro laso RU: self defense or

just business as US

Pentagon

officials are concerned US stealth

jets and satellites at risk from Russia's next-generation system.

….

FACT: BOTH OF THEM are putting the world peace at risk: one

mistake &..

====

SPUTNIK and RT SHOWS

GEO-POL n GEO-ECO

..Focus on neoliberal expansion via wars & danger of WW3

Look who is talking on “decency” ..

-Kingsnake

Receives Assist After Attempting to Devour Itself There won’t be Ass f-T

----

----

NOTICIAS IN SPANISH

Lat Am search f alternatives to neo-fascist regimes &

terrorist imperial chaos

REBELION

Mund Trump ordenó atacar a Iran y, tras girar la

cabeza 360º como la niña del exorcista, dijo “Stop” Javier

C Si la gira de nuevo..se auto-devora como l Serpiente

Mund Todos los caminos de Trump conducen

a China Guadi Calvo No lo creo: T

y su Team (TTs) no saben adónde van, solo que hay que producir más armas y

venderlas para dar vida al terror imperial..Si eso causa el WW3 y US es hit,

los TTs dirán fue RU y los Chinos vendrán a ayudar en la reconstrucción y

pasaran la cuenta a los billonarios y si no pueden pagar, se quedaran con sus

bancos y sus empresas, ‘según pre-contrato’. Y si incumplen, serán China y RU

quienes les den el bombazo final. El camino es al US.

===

ALAI ORG

BLOCKED

====

RT EN

ESPAÑOL

- La receta de un expresidente español para "acabar ya" con Maduro

- Trump avisa: "Un ataque de Irán será recibido con fuerza abrumadora" y "la aniquilación de algunas áreas"

- Argentina desarrolla un nuevo tratamiento para el VIH: ¿de qué se trata?

- China acapara oro y vende sus activos en dólares

- Huawei plantea a la India un pacto contra la filtración de datos

- El curioso cambio en el reglamento de la fase final de la Copa América 2019

- La terrible imagen que indigna al mundo: un migrante salvadoreño y su bebé mueren abrazados cuando intentaban llegar a EE.UU.

- EE.UU.: Aprueban un proyecto de ley de 4.500 millones de dólares para enfrentar a la crisis humanitaria en la frontera

- Así de catastróficas serán las consecuencias para la economía mundial si se produce un conflicto armado entre EE.UU. e Irán

- Exjefe del SEBIN se esconde en EE.UU. tras el fallido intento de golpe en Venezuela

- Descubren cómo el café ayuda a quemar grasas y adelgazar

- Un asteroide del tamaño de tres campos de fútbol se aproximará este jueves a la Tierra

- El "acuerdo del siglo" de EE.UU. sobre Palestina, ¿una excusa frente a la autodeterminación?

- La India reafirma su decisión de adquirir sistemas S-400 rusos durante la visita de Pompeo

- Keiser Report La estafa Ponzi alimentada con dinero de los contribuyentes más humildes

- Cartas sobre la mesa México: ¿se puede asegurar la paz mediante las armas?

Por supuesto: armar la paz es justicia,

autodeterminación y soberanía. El único problema es cuando declararla

públicamente. Pero armarla: desde ahora! Si ocurre el WW3 se estaría prepar para evitar otra

expropiac de territ.. y para ..

----

----

INFORMATION

CLEARING HOUSE

Deep on the

US political crisis: neofascism & internal conflicts that favor WW3

U.S. Citizens Would Approve Preventive

Nuclear Strike On North Korea

By Moon Of Alabama. Solo un tercio según datos oficiales. Pero eso es ya más que la población de N-Korea. El problema es que US nunca sufrió lo que paso en Hiroshima y Nagazaki. Esta vez hay evidencias de que si será bombardeado. Y cuando eso ocurra muere el patrioterism y es el “sálvese quien pueda” lo que viene. N-K debe prepararse para golpear sitios claves de la OTAN a su alcance. Jamás debe entregar sus armas. Get new ones, instead. Si hay que morir, hay que hacerlo de pie, no de rodillas.

By Moon Of Alabama. Solo un tercio según datos oficiales. Pero eso es ya más que la población de N-Korea. El problema es que US nunca sufrió lo que paso en Hiroshima y Nagazaki. Esta vez hay evidencias de que si será bombardeado. Y cuando eso ocurra muere el patrioterism y es el “sálvese quien pueda” lo que viene. N-K debe prepararse para golpear sitios claves de la OTAN a su alcance. Jamás debe entregar sus armas. Get new ones, instead. Si hay que morir, hay que hacerlo de pie, no de rodillas.

….

You Are Being Trolled By Dmitry Orlov What do you think will happen when the

next financial collapse hits? Esta víspera es mas cercana que el

WW3, pero es esto lo que viene inmediatamente

luego del colapso económico. Eso lo saben todos.. no el pueblo americano. In Short: we’re not

ready for WW3,, only billionaires have bunkers, no you..

….

….

….

….

….

The Diminishing American Economy By Paul Craig Roberts

….

The Geopolitics of World War III By StormCloudsGathering

….

---

COUNTER

PUNCH

Analysis on

US Politics & Geopolitics

Rannie Amiri Instigators

of a Persian Gulf Crisis

Patrick Cockburn Trump

May Already be in Too Deep to Avoid War With Iran

John Feffer Deep

Fakes: Will AI Swing the 2020 Election?

Binoy Kampmark Bill

Clinton in Kosovo

Jim Kavanagh Eve

of Destruction: Iran will Strike Back

----

----

GLOBAL

RESEARCH

Geopolitics

& Econ-Pol crisis that leads to more business-wars from US-NATO allies

-Beyond

Climate Tipping Points: Greenhouse Gas Levels Exceed the Stability Limit of the

Greenland and Antarctic Ice Sheets By Dr. Andrew Glikson,

-Most

Democratic Candidates Still Afraid to Criticise Israel’s Violations of

Palestinian Rights By James J. Zogby

----

----

DEMOCRACY NOW

Amy Goodman’ team

----

----

PRESS TV

Resume of Global News described

by Iranian observers..

----

===

No hay comentarios:

Publicar un comentario